Now Reading: The Luxury Paradigm: How India’s Metro Cities Are Redefining Ultra-High-End Real Estate Investment Returns

-

01

The Luxury Paradigm: How India’s Metro Cities Are Redefining Ultra-High-End Real Estate Investment Returns

The Luxury Paradigm: How India’s Metro Cities Are Redefining Ultra-High-End Real Estate Investment Returns

India’s luxury real estate sector has entered an unprecedented golden age, with metropolitan markets delivering exceptional returns that rival—and often exceed—global luxury property destinations. The luxury housing segment, defined as properties priced at ₹4 crore and above, has demonstrated remarkable resilience and growth, recording an extraordinary 85% year-on-year surge in H1 2025, with approximately 7,000 units sold across the top seven cities.

This represents not merely a market correction but a fundamental shift in India’s wealth creation narrative, positioning luxury real estate as the preferred asset class for the country’s expanding cohort of 85,698 High Net Worth Individuals (HNWIs) and 191 billionaires.

What returns can investors expect from luxury real estate in Indian metros?

Prime luxury property in Mumbai, Delhi, and Bengaluru has delivered 8-12% annual appreciation over the past decade, with rental yields of 2-4%. Total returns compare favourably to equity markets on a risk-adjusted basis for long-term investors.

Which Indian metro city offers the best luxury real estate investment returns?

Mumbai consistently leads in luxury property appreciation, followed by Delhi NCR and Bengaluru. Hyderabad has the fastest-growing luxury segment. Location within the city matters more than the city itself – micro-market selection is critical.

How has the luxury real estate market in India changed post-COVID?

Post-COVID luxury demand shifted toward larger homes, private outdoor spaces, and smart features. Buyers prioritised wellness amenities, home offices, and low-density developments. Prices in prime locations rose 20-35% between 2022 and 2025.

What is the outlook for luxury real estate in Indian metros for 2026?

Analysts project 8-12% price appreciation for prime luxury properties in 2026, driven by strong NRI demand, UHNI wealth growth, and limited prime land supply. The Rs 10 Cr+ segment is expected to outperform the broader residential market.

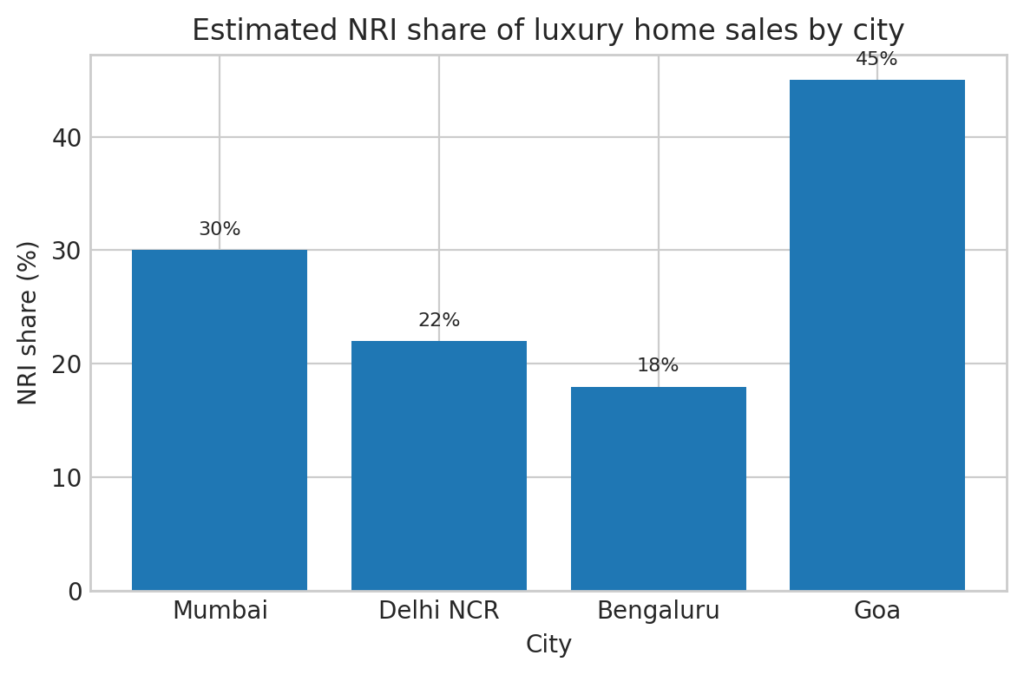

Related reading: NRI real estate investment guide — legal framework, financing, and market selection.

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post