Now Reading: NRI Property Buying Process India: Essential Step-by-Step Guide 2026

-

01

NRI Property Buying Process India: Essential Step-by-Step Guide 2026

Table of Contents

- NRI Property Buying Process India: Complete Overview

- Who Qualifies as an NRI for Property Purchase?

- FEMA Rules for NRI Property Investment

- Step-by-Step NRI Property Buying Process India

- NRI Home Loan Options and Comparison

- State-Wise Stamp Duty Table for NRIs

- Double Taxation Avoidance Agreements (DTAA)

- Repatriation of Sale Proceeds — Complete Walkthrough

- Tax Obligations for NRI Property Owners

- Due Diligence Checklist for NRI Buyers

- 7 Common Scams Targeting NRI Property Buyers

- Power of Attorney for NRI Property Transactions

- Post-Purchase Management

- Frequently Asked Questions

- Get NRI Property Advisory

NRI Property Buying Process India: Complete Overview

The NRI property buying process India involves navigating a unique set of regulations that differ from those applicable to resident Indians. Non-Resident Indians and Persons of Indian Origin have specific rights and restrictions under FEMA (Foreign Exchange Management Act) that govern what they can buy, how they can pay, and how they can repatriate sale proceeds.

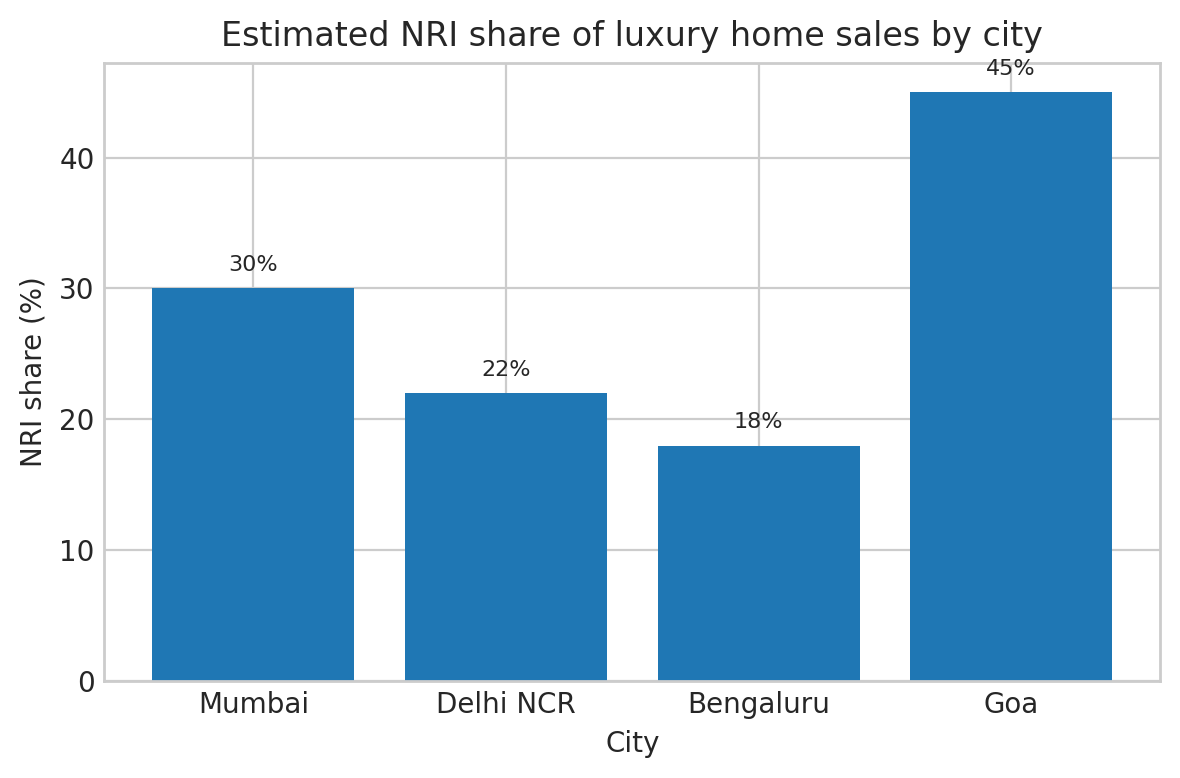

India remains one of the most attractive real estate markets for NRI investors. Favourable exchange rates, strong capital appreciation in key markets, emotional connections to homeland, and retirement planning all drive NRI property purchases. In 2024, NRI investment in Indian real estate reached approximately USD 14.9 billion (over Rs 1.2 lakh crore), with projections for 2025 crossing USD 16 billion. Goa, Mumbai, Bangalore, and Hyderabad remain the top destinations.

However, the process is significantly more complex than a domestic purchase. Different account types (NRE, NRO, FCNR), TDS obligations, repatriation limits, and Power of Attorney requirements all add layers of complexity. This guide walks you through every step of the NRI property buying process India, from initial eligibility check to post-purchase management.

For Goa-specific market insights, visit our Goa real estate page.

Who Qualifies as an NRI for Property Purchase?

Understanding your legal status is the first step in the NRI property buying process India. The definition of NRI varies between FEMA (for foreign exchange purposes) and the Income Tax Act (for tax purposes).

FEMA Definition (for property purchase)

Under FEMA, a person is considered an NRI if they are an Indian citizen residing outside India. Additionally, Persons of Indian Origin (PIOs) and Overseas Citizens of India (OCI) cardholders have property purchase rights similar to NRIs, with some restrictions.

- NRI (Indian passport holder): Can buy residential and commercial property without limit. Cannot buy agricultural land, plantation property, or farmhouse.

- OCI cardholder: Same rights as NRI for residential and commercial property. Cannot buy agricultural land, plantation property, or farmhouse.

- PIO: Same rights as NRI. The PIO category has been merged with OCI since 2015.

- Foreign national (non-Indian origin): Generally cannot buy immovable property in India. Special permission required from RBI.

Income Tax Definition (for tax purposes)

For income tax, residential status depends on the number of days spent in India during the financial year. An individual is a non-resident if they spend less than 182 days in India during the year (or less than 120 days if Indian income exceeds Rs 15 lakh). Tax treatment of rental income, capital gains, and TDS depends on this classification.

Your FEMA status determines what you can buy. Your Income Tax status determines how you are taxed. These are independent classifications, and you should verify both before proceeding.

FEMA Rules for NRI Property Investment

FEMA governs all foreign exchange transactions in India, including NRI property purchases. The RBI FEMA guidelines set out the rules clearly. Here are the key provisions.

What NRIs Can Buy

- Residential property: No limit on the number of properties. No RBI permission required.

- Commercial property: No limit on the number of properties. No RBI permission required.

- Agricultural land, plantation property, farmhouse: Cannot be purchased. These can only be acquired through inheritance or as a gift from a person resident in India.

How NRIs Can Pay

Payment for property must be made through specific channels:

- NRE (Non-Resident External) account: Funded by foreign earnings. Fully repatriable. Interest is tax-free in India.

- NRO (Non-Resident Ordinary) account: Funded by Indian earnings (rent, dividends, etc.). Repatriation limited to USD 1 million per financial year.

- FCNR (Foreign Currency Non-Resident) account: Fixed deposit in foreign currency. Fully repatriable.

- Home loan from Indian bank: Disbursed in Indian rupees. Available from most major banks.

Important: Payment cannot be made in foreign currency, travellers’ cheques, or through a person resident outside India. All payments must flow through Indian banking channels.

Joint Purchase Rules

An NRI can jointly purchase property with another NRI or a person resident in India. However, a person resident in India cannot jointly purchase property with a foreign national (non-Indian origin) without RBI permission.

Step-by-Step NRI Property Buying Process India

Here is the complete NRI property buying process India, broken down into clear stages.

Stage 1: Preparation (4–8 weeks before purchase)

- Open NRE/NRO account: If you do not already have one, open an NRE or NRO account with an Indian bank. This is mandatory for routing property payments.

- Obtain PAN card: A PAN card is required for all property transactions in India. Apply online if you do not have one.

- Arrange Power of Attorney (if needed): If you cannot be present in India for the transaction, execute a Power of Attorney in favour of a trusted person. The PoA must be notarised and apostilled in your country of residence.

- Set budget and location: Research property markets, prices, and locations. For Goa, use our Goa property prices 2026 guide.

Stage 2: Property Selection (2–6 weeks)

- Shortlist properties: Use online portals, local agents, and advisory services to identify suitable properties.

- Verify RERA registration: For under-construction projects, confirm RERA registration on the state portal. See our RERA approved projects in Goa guide.

- Site visit: If possible, visit the property in person. If not, arrange a video walkthrough and independent inspection.

- Legal due diligence: Engage a local lawyer to verify title, encumbrances, approvals, and compliance. This is critical and should not be skipped.

Stage 3: Agreement and Payment (2–4 weeks)

- Negotiate and agree on terms: Price, payment schedule, possession date, and specifications.

- Sign the agreement for sale: This can be done in person or through PoA. Pay stamp duty on the agreement.

- Make payments through NRE/NRO/FCNR account: All payments must be traceable through banking channels. Keep records of every transfer.

- Apply for home loan (if needed): Indian banks offer NRI home loans with specific documentation requirements.

Stage 4: Registration (1–2 weeks)

- Pay stamp duty and registration fees: Rates vary by state. See the stamp duty table below.

- Execute and register the sale deed: Done at the Sub-Registrar’s office. Both buyer and seller (or their PoA holders) must be present.

- Collect registered documents: The registered sale deed is your primary proof of ownership.

Stage 5: Post-Purchase (Ongoing)

- Mutation of property records: Apply for mutation at the local municipal body to update ownership records.

- Utility transfers: Transfer electricity, water, and gas connections to your name.

- Property management: Arrange for maintenance and rental management if not residing in India.

- Tax compliance: File Indian income tax returns if you earn rental income or sell the property.

NRI Home Loan Options and Comparison

Most major Indian banks offer home loans to NRIs. Here is an indicative comparison of key terms. Note: Interest rates change frequently based on RBI policy, credit score, and loan amount. Always confirm the latest rates directly with the bank before applying.

| Bank | Interest Rate (Starting From) | Max LTV | Max Tenure | Processing Fee |

|---|---|---|---|---|

| SBI | 8.00%–8.50% onwards | 80% | 30 years | 0.35% of loan amount |

| HDFC Bank | 8.15% onwards | 75–90% | 20 years | 0.50% of loan amount |

| ICICI Bank | 8.75% onwards | 80% | 20 years | 0.50% of loan amount |

| Axis Bank | 8.75% onwards | 80% | 20 years | Up to 1% of loan amount |

| Bank of Baroda | 8.40% onwards | 80% | 30 years | 0.25% of loan amount |

| PNB Housing | 8.90% onwards | 75% | 20 years | 0.50% of loan amount |

Key NRI home loan requirements:

- Valid Indian passport and OCI/PIO card (if applicable)

- Employment proof from country of residence (minimum 2 years stability)

- Bank statements from overseas account (12 months)

- Income proof — salary slips, tax returns from country of residence

- PAN card and Aadhaar (if available)

- Property documents (agreement for sale, approved plans, title deed)

NRI-specific loan conditions:

- Loan disbursement is in Indian rupees, credited to the NRE/NRO account

- EMI repayment must be through NRE/NRO account

- Some banks require a resident Indian co-applicant

- Interest rates for NRIs are typically 0.25–0.50% higher than for residents

- Loan tenure may be capped at the borrower’s retirement age

State-Wise Stamp Duty Table for NRIs

Stamp duty varies significantly across Indian states. This table covers the major states where NRIs commonly invest.

| State | Stamp Duty (Male) | Stamp Duty (Female) | Registration Fee | Total (Approx.) |

|---|---|---|---|---|

| Goa | 3.5%–6% | 3.5%–6% | 1% | 4.5%–7% |

| Maharashtra | 6% (7% in metro areas incl. metro cess) | 5% (6% in metro areas) | 1% | 6%–8% |

| Karnataka | 5% | 5% | 1% | 6% |

| Kerala | 8% | 8% | 2% | 10% |

| Tamil Nadu | 7% | 7% | 4% | 11% |

| Delhi | 6% (+1% surcharge above Rs 25 lakh) | 4% (+1% surcharge above Rs 25 lakh) | 1% | 5%–8% |

| Telangana | 6% | 6% | 0.5% | 6.5% |

| Rajasthan | 6% | 5% | 1% | 6%–7% |

| Uttar Pradesh | 7% | 6% | 1% | 7%–8% |

Goa offers one of the lowest stamp duty rates in India, making it a cost-efficient state for NRI property investment. This is one of the factors driving NRI interest in the Goa real estate market.

Double Taxation Avoidance Agreements (DTAA)

A critical but often overlooked aspect of the NRI property buying process India is the Double Taxation Avoidance Agreement (DTAA). India has DTAA treaties with over 90 countries, which prevent NRIs from being taxed twice on the same income.

How DTAA Applies to Property Income

If you earn rental income or capital gains from Indian property, both India and your country of residence may claim taxation rights. DTAA treaties determine which country has primary taxation rights and how to claim credit for taxes paid in the other country.

Rental income: Under most DTAA treaties, rental income from Indian property is taxable in India. You can then claim a tax credit in your country of residence for taxes paid in India, avoiding double taxation.

Capital gains: Capital gains from Indian property are generally taxable in India. You can claim foreign tax credit in your country of residence. The specific mechanism depends on the treaty between India and your country.

DTAA and Key NRI Countries

- USA: India-US DTAA allows tax credit for Indian taxes against US tax liability. Report Indian property income on Form 1116 (Foreign Tax Credit).

- UK: India-UK DTAA provides credit relief. Indian taxes can be offset against UK tax on the same income.

- UAE: India-UAE DTAA exists, but UAE does not levy income tax. Indian income is taxed in India with no double taxation issue.

- Canada: India-Canada DTAA allows foreign tax credit mechanism. Canadian residents report worldwide income and claim credit for Indian taxes.

- Australia: India-Australia DTAA provides similar foreign tax credit provisions.

- Singapore: India-Singapore DTAA allows credit for Indian taxes against Singapore tax liability.

Always consult a chartered accountant specialising in international taxation to optimise your tax position under DTAA. File returns in both countries to claim the appropriate credits. For Indian tax filing, use the Income Tax India e-filing portal.

Repatriation of Sale Proceeds — Complete Walkthrough

One of the most complex aspects of the NRI property buying process India is repatriating sale proceeds when you sell the property. The rules differ depending on whether the property was purchased with repatriable funds (NRE/FCNR) or non-repatriable funds (NRO).

Properties Purchased with NRE/FCNR Funds

If you bought the property entirely with NRE or FCNR funds:

- Sale proceeds (up to the original purchase amount in foreign exchange terms) can be repatriated freely

- No RBI permission required for repatriation

- Maximum 2 residential properties can be repatriated under this route

- The property must have been held for at least 10 years (removed in 2015 — now no holding period restriction)

- Capital gains above the original investment can be repatriated through the NRO route (up to USD 1 million per year)

Properties Purchased with NRO Funds

If you bought the property with NRO funds or Indian income:

- Sale proceeds can be repatriated up to USD 1 million per financial year

- This limit includes all NRO remittances (not just property sale proceeds)

- Form 15CA and 15CB must be filed for each remittance

- A chartered accountant certificate (Form 15CB) is required

- Tax clearance is required — all capital gains tax must be paid before repatriation

Step-by-Step Repatriation Process

- Complete the sale: Register the sale deed and receive payment into your NRO account.

- Pay capital gains tax: The buyer deducts TDS (12.5% for long-term capital gains, 30% for short-term capital gains, as per 2024 Budget amendments). Ensure TDS is deposited correctly.

- Obtain CA certificate: Engage a chartered accountant to issue Form 15CB, certifying that taxes have been paid and repatriation is permissible.

- File Form 15CA online: File this form on the Income Tax e-filing portal before initiating the remittance.

- Apply to your bank: Submit the repatriation request to your bank along with Form 15CA, 15CB, sale deed copy, TDS certificates, and your tax returns.

- Bank processes remittance: The bank verifies documents and processes the foreign exchange remittance to your overseas account.

Timeline: The entire repatriation process typically takes 2–4 weeks after the sale is completed, assuming all documentation is in order.

Tax Obligations for NRI Property Owners

NRIs owning property in India have specific tax obligations that must be fulfilled annually.

Rental Income Tax

- Rental income is taxable at slab rates applicable to NRIs

- Standard deduction of 30% of gross rental income is available

- Home loan interest deduction available under Section 24(b) — up to Rs 2 lakh for self-occupied, no limit for let-out property

- Tenant must deduct TDS at 30% (plus surcharge and cess) on rent paid to an NRI. The tenant deposits this with the government.

- NRI can file returns and claim refund if actual tax liability is lower than TDS deducted

Capital Gains Tax on Sale

- Short-term (less than 2 years): Taxed at applicable slab rates. TDS at 30%.

- Long-term (more than 2 years): Taxed at 12.5% without indexation (post-July 2024 Budget). For properties acquired before 23 July 2024, resident individuals and HUFs can opt for 20% with indexation if it results in a lower tax liability.

- Exemption under Section 54: Reinvest gains in another residential property within 2 years

- Exemption under Section 54EC: Invest gains in specified bonds (NHAI, REC) within 6 months — maximum Rs 50 lakh

TDS on Property Sale by NRI

When an NRI sells property, the buyer must deduct TDS at 12.5% of the sale consideration (for long-term capital gains, as per the July 2024 Budget) or 30% (for short-term capital gains), plus applicable surcharge and cess. This is significantly higher than the 1% TDS applicable when a resident sells property.

NRIs can apply for a lower TDS certificate from the Assessing Officer if their actual tax liability is lower. This involves filing Form 13 with the Income Tax department.

Due Diligence Checklist for NRI Buyers

NRI buyers face higher risks than resident buyers due to physical distance and limited ability to oversee transactions personally. This checklist covers every verification point in the NRI property buying process India.

Legal Verification

- Title deed verification (minimum 30-year chain of ownership)

- Encumbrance certificate (free from liens, mortgages, and charges)

- Survey records and property boundaries match ground reality

- No pending litigation involving the property or the land

- Approved building plan from the local authority

- RERA registration (for under-construction projects)

- CRZ clearance (for coastal properties)

- Conversion order (if agricultural land is being converted)

- No government acquisition orders pending on the land

Financial Verification

- Property value matches the circle rate or guidance value

- Payment schedule aligns with construction milestones (for under-construction)

- All payments routed through NRE/NRO/FCNR accounts

- TDS provisions are correctly factored into the payment

- Home loan pre-approval obtained (if financing)

- Stamp duty and registration costs budgeted

Physical Verification

- Physical inspection of the property (in person or via video)

- Verification that construction matches approved plans

- Assessment of neighbourhood, road access, and infrastructure

- Quality of construction materials and workmanship

- Availability of water, electricity, and sewage

For a broader investment strategy, consult our smart home investment guide.

7 Common Scams Targeting NRI Property Buyers

NRIs are particularly vulnerable to property scams due to their physical absence from India. Here are the most common scams and how to protect yourself.

1. Title Fraud

Fraudsters sell property they do not own, using forged documents. They target NRIs because verification from overseas is harder. Protection: Always hire an independent lawyer to verify the title chain. Do not use the seller’s recommended lawyer.

2. Power of Attorney Misuse

A person holding your PoA may misuse it to sell, mortgage, or encumber your property without your knowledge. Protection: Use a specific (not general) PoA with limited powers. Include an expiry date. Revoke immediately after the transaction is complete.

3. Inflated Pricing

Agents may quote significantly higher prices to NRIs, knowing they are less familiar with local market rates. Protection: Research market rates independently. Use multiple sources. Compare with the government circle rate.

4. Fake RERA Registration

Some developers claim RERA registration with fake or expired numbers. Protection: Verify every RERA number directly on the state RERA portal. Do not accept screenshots or certificates from the developer alone.

5. Advance Fee Fraud

Fraudsters collect advance payments (token money) for properties they have no authority to sell. They disappear after collecting the advance. Protection: Never pay advances without verifying ownership and signing a formal agreement. Route all payments through banking channels.

6. Encumbered Property Sale

Properties with existing loans, mortgages, or legal disputes are sold without disclosure. The NRI buyer discovers the encumbrance only after registration. Protection: Obtain a fresh encumbrance certificate directly from the Sub-Registrar’s office. Verify for the past 30 years.

7. Under-Reporting of Sale Value

Sellers may pressure NRI buyers to agree to a lower registered value (to reduce stamp duty) while paying the balance in cash. This is illegal and creates problems during repatriation. Protection: Always register the full transaction value. Underpayment of stamp duty is detectable and can lead to penalties and criminal charges.

Power of Attorney for NRI Property Transactions

Most NRIs cannot be physically present in India for every step of the property purchase. A Power of Attorney allows a trusted person to act on your behalf. Here is how to execute a valid PoA for property transactions.

Types of PoA

- General Power of Attorney (GPA): Grants broad powers to the agent. Higher risk of misuse. Avoid for property transactions if possible.

- Special Power of Attorney (SPA): Grants specific, limited powers for a defined transaction. Recommended for property purchases.

Execution Process

- Draft the PoA: Have a qualified Indian lawyer draft the PoA with specific powers related to your property transaction. Include the property details, permitted actions, and expiry date.

- Notarise in your country: Sign the PoA before a notary public in your country of residence. Ensure proper identification and witness requirements are met.

- Apostille or attest: For countries that are part of the Hague Convention, get an Apostille stamp. For non-Hague countries, attest through the Indian consulate or embassy.

- Send to India: Courier the original PoA to your agent in India.

- Adjudication: The PoA must be adjudicated (stamped) in India within 3 months of execution. Take it to the Collector’s office or Sub-Registrar for adjudication.

Cost: Notarisation fees vary by country (typically USD 50–200). Apostille fees are usually USD 10–50. Adjudication in India involves nominal stamp duty.

For a comprehensive overview of the buying process in Goa specifically, visit our NRI real estate investment guide.

Post-Purchase Management

Managing property from overseas requires reliable systems and trusted local partners. Here are the key post-purchase activities in the NRI property buying process India.

Property Management

If you plan to rent out the property, consider hiring a professional property management company. They handle tenant sourcing, rent collection, maintenance, and compliance. Fees typically range from 8–15% of rental income.

Mutation and Records Update

After registration, apply for mutation at the local municipal body (Panchayat in rural Goa, Corporation in urban areas). Mutation updates the revenue records to reflect your ownership. Without mutation, you may face issues with property tax bills and future sales.

Property Tax

Pay annual property tax to the local municipal body. Rates vary by location and property type. Set up auto-payment or instruct your property manager to handle this. Unpaid property tax accumulates interest and can result in penalties.

Insurance

Property insurance is not mandatory in India but is strongly recommended. Cover the property against fire, natural disasters, and theft. Annual premiums are typically 0.1–0.3% of the property value.

Annual Tax Filing

File Indian income tax returns annually if you earn rental income or have any Indian income exceeding the basic exemption limit. Use the Income Tax India e-filing portal to file returns online.

Frequently Asked Questions

Can NRIs buy property in India without visiting the country?

Yes. The NRI property buying process India can be completed entirely through a Power of Attorney. However, a personal visit for property inspection is strongly recommended for due diligence purposes.

How many properties can an NRI buy in India?

There is no limit on the number of residential or commercial properties an NRI can purchase in India. However, NRIs cannot buy agricultural land, plantation property, or farmhouses.

Can an NRI get a home loan in India?

Yes. Most major Indian banks — SBI, HDFC, ICICI, Axis, Bank of Baroda — offer home loans to NRIs. The LTV ratio is typically 75–80%, and interest rates are marginally higher than resident rates.

What is the TDS rate when an NRI sells property?

The buyer must deduct TDS at 12.5% (plus surcharge and cess) for long-term capital gains and 30% (plus surcharge and cess) for short-term capital gains, as per the July 2024 Budget amendments. This is significantly higher than the 1% TDS for resident sellers.

Can NRIs repatriate property sale proceeds?

Yes. If the property was purchased with NRE/FCNR funds, the purchase amount (in foreign exchange terms) can be repatriated freely for up to 2 properties. Sale proceeds from NRO-funded purchases can be repatriated up to USD 1 million per financial year.

Is it safe for NRIs to invest in Indian property?

With proper due diligence, legal verification, and professional advisory, Indian property investment is generally safe for NRIs. RERA has significantly improved buyer protections. The key risks — title fraud, encumbrances, and project delays — can all be mitigated through thorough verification.

What happens to NRI property in India after death?

NRI property in India is governed by Indian succession laws. It can be inherited by legal heirs (under the Hindu Succession Act, Indian Succession Act, or Muslim Personal Law, depending on religion). NRIs should have a valid Indian will covering their Indian assets.

Can an NRI gift property in India?

Yes. An NRI can gift residential or commercial property to a person resident in India or another NRI. Gift tax provisions under the Income Tax Act apply. Gifts to specified relatives are exempt from tax.

Which Indian cities offer the best returns for NRI investors?

Goa, Hyderabad, Bangalore, and Pune have shown the strongest appreciation combined with rental yields over the past five years. Goa specifically offers 5–8% rental yields and 10–18% annual appreciation in premium areas. See our best areas to buy property in Goa guide for details.

Get NRI Property Advisory

The NRI property buying process India is complex, but it does not have to be overwhelming. Our team at Proptys specialises in guiding NRI buyers through every step — from initial property search to registration, tax compliance, and property management.

We understand the unique challenges NRIs face: time zone differences, reliance on third parties, complex documentation, and the need for trustworthy local representation. Our end-to-end advisory service is designed specifically for NRI buyers investing in Goa and other Indian markets.

Services include property search and shortlisting, legal due diligence, RERA verification, PoA guidance, home loan coordination, registration assistance, and post-purchase property management.

Contact Proptys today for a free NRI property advisory consultation. Tell us your requirements, and we will create a personalised investment plan for you.

Summary: NRI Property Buying Process India

The NRI property buying process India is a structured, well-regulated path that thousands of NRIs successfully navigate every year. From verifying your eligibility under FEMA to completing registration through a Power of Attorney, every stage of the NRI property buying process India has clear guidelines and legal safeguards.

Before you begin the NRI property buying process India, open an NRE or NRO account, engage a DTAA-aware tax advisor, and appoint a local lawyer experienced in the state where you plan to buy. The NRI property buying process India rewards thorough preparation.

Whether you are purchasing your first property or expanding an existing portfolio, the NRI property buying process India offers strong legal protections through RERA, FEMA compliance frameworks, and the Indian judiciary. Start your NRI property buying process India with confidence by following the steps outlined in this guide.

NRI Investment in India Real Estate — RBI Guidelines

The Reserve Bank of India’s framework for NRI investment in India real estate is governed by FEMA (Foreign Exchange Management Act) regulations and is materially identical to resident citizen treatment for residential and commercial property. Key RBI guidelines for NRI investment include: payment must route through NRE/NRO/FCNR accounts (no direct foreign currency); agricultural land, farmhouses and plantation properties require RBI approval; repatriation of sale proceeds is capped at USD 1 million per financial year per person from NRO funds, with no cap on NRE-funded purchases.

NRIs can hold an unlimited number of residential and commercial properties in India. Joint ownership with another NRI or a resident family member is permitted. Inheritance of any property type — including agricultural land — is allowed, though continued holding of agricultural land may require regularisation. For comprehensive context on the broader regulatory and strategy landscape, see our NRI real estate investment in India strategy guide.

Real Estate Investment in India for NRI — Property Types Allowed

Permitted: residential apartments, villas, plotted residential land (urban), commercial property (offices, retail, shops, warehouses), branded residences, and units in REITs and listed AIFs. Restricted (need RBI approval): agricultural land, plantation property, farmhouses. The Power of Attorney route allows full transaction completion from abroad — registration in India must follow Consular attestation in the country of residence.

For premium luxury property in India and Sri Lanka curated for NRI investors, see listiing.com — including freehold villas in Goa and fractional ownership at Altaira (Sri Lanka).

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post