Now Reading: Beyond Net Zero: India’s Regenerative Luxury Estates Are Redrawing the Map of Wealth

-

01

Beyond Net Zero: India’s Regenerative Luxury Estates Are Redrawing the Map of Wealth

Beyond Net Zero: India’s Regenerative Luxury Estates Are Redrawing the Map of Wealth

India’s luxury property market is moving past prestige for prestige’s sake. A new buyer class—UHNIs, HNIs, global Indians, and family offices—is now chasing estates that do more than conserve value: they restore land, reduce operational drag, and signal cultural permanence. Knight Frank’s 2025 Wealth Report says India’s HNIs rose to 85,698 in 2024 and are projected to reach 93,753 by 2028, while UHNWIs climbed from 13,263 in 2023 to 19,908 by 2028 .

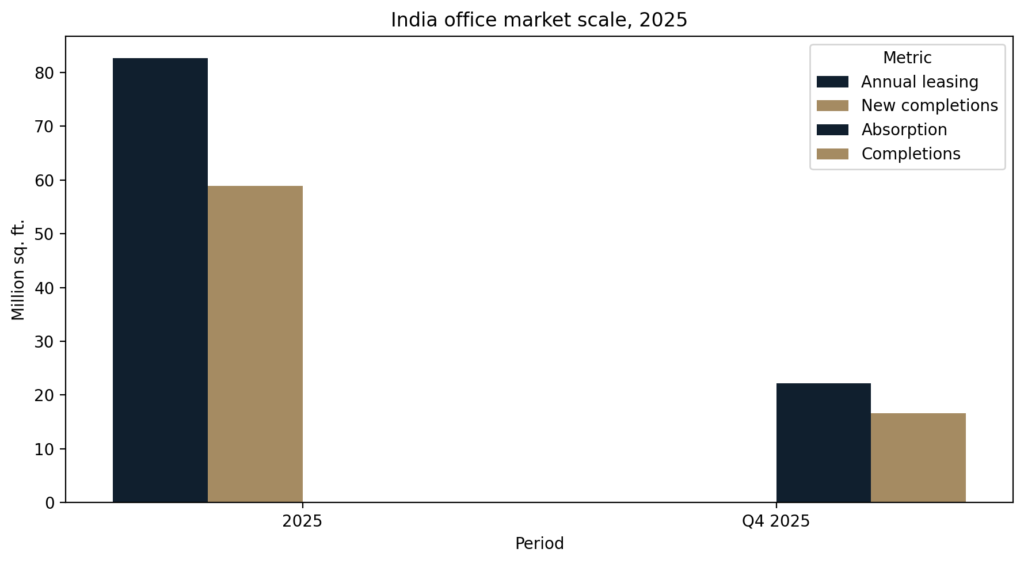

CBRE says India’s office market also set a record in 2025, with 82.6 million sq. ft. leased and 93% of new completions green-certified in Q4, underscoring how sustainability has become a default expectation, not a premium add-on. For capital seeking regenerative luxury estate exposure, the opportunity is no longer only in Mumbai or Delhi, but in a widening wealth geography shaped by Bengaluru, Hyderabad, Pune, Chennai, Goa, and select Himalayan and coastal enclaves.

Shifting Market Dynamics and Global Context

The global context is clear: wealth is becoming more selective, more mobile, and more sensitive to quality. Knight Frank’s Wealth Report 2025 notes that 44% of family offices plan to increase real estate allocations, and that direct property already averages 22.5% of a typical family office portfolio. That matters because luxury housing is no longer simply a consumption category; it is increasingly treated as a strategic store of value, lifestyle infrastructure, and intergenerational capital.

In India, this has converged with a structural premiumization of residential demand, where JLL said 2025 saw an 11% decline in total sales but a 6% rise in sales of INR 1 crore+ apartments, showing that value is concentrating in the top end rather than broadening evenly.

Evidence and Market Signals

The numbers support the shift. Knight Frank reported India’s HNI population at 85,698 in 2024, up 6% from 2023, and projected it to reach 93,753 by 2028. It also said India had 191 billionaires in 2024, up 12% year-on-year, which is one of the clearest signals of domestic capital formation at the top . CBRE reported 2025 office leasing at 82.6 million sq. ft., a record level and a proxy for the confidence of occupiers, investors, and developers in India’s premium urban ecosystems .

On the investment side, CBRE said equity inflows into India’s real estate market reached over USD 14 billion in 2025, an all-time high, reflecting deeper institutional conviction. Anarock-related reporting showed housing sales across the top seven cities fell 14% in 2025, yet total value rose 6% to above INR 6 lakh crore, with nearly 21% of new supply launched above INR 2.5 crore; the market is getting more expensive even when volumes soften.

Lifestyle Aspirations and Emotional Appeal

The appeal of regenerative estates is partly financial, but the emotional logic is deeper. Wealthy families are increasingly looking for homes that make a statement about stewardship rather than excess. That means larger plots, privacy, low-density neighborhoods, water sensitivity, edible landscapes, solar autonomy, wellness architecture, and materials that age with dignity.

Knight Frank’s 2025 report highlights sustainability and younger investor preferences as defining themes, which helps explain why luxury buyers are moving toward homes that feel both exclusive and morally legible. In practice, this is the difference between a trophy asset and a place that can host family, work, retreat, and renewal in one address.

Case Studies

Goa’s low-density luxury

Goa remains a compelling case for regenerative luxury because it combines scarcity, lifestyle value, and high emotional utility. Demand here is not just about sea views; it is about a slower civic tempo, design privacy, and the ability to own land in a market where buildable supply is tight. Knight Frank’s luxury demand framework and CBRE’s sustainability trend both help explain why buyers now value low-density, green-certified, lifestyle-led properties over conventional high-rise prestige.

For a useful market lens, see Knight Frank Wealth Report 2025 and CBRE India Office Figures Q4 2025. For UHNI buyers, Goa is becoming a second-home market with a stronger identity than a purely speculative one.

Bengaluru’s wealth engine

Bengaluru has emerged as a high-conviction city because it combines HNI formation, GCC growth, and premium consumption. CBRE said Bengaluru, Mumbai, and Delhi-NCR accounted for about 61% of total office take-up in 2025, while GCCs accounted for 39% of Q4 absorption, confirming the city’s role in wealth creation and housing demand.

Delhi-NCR and super-prime land

Delhi-NCR still matters because it is where land, legacy, and status intersect. ANAROCK-related reporting in 2025 showed clear momentum in high-ticket homes, with the luxury segment becoming a larger share of transactions and the ultra-luxury segment rising sharply in value terms . That makes NCR especially relevant for buyers thinking in terms of enclave living, private gardens, larger floorplates, and future intergenerational transfer.

For market context, ANAROCK housing market reporting and related coverage in the business press suggest that the value pool is moving upward even when transaction counts moderate. In NCR, the question is no longer whether luxury exists, but which micro-market can preserve discretion and scarcity best.

Investor Priorities

- Build an UHNI portfolio diversification strategy around scarce land, not just finished apartments.

- Prioritize cities where wealth creation and end-user demand overlap, especially Bengaluru, Hyderabad, Pune, Goa, and select NCR micro-markets.

- Treat green certification as a pricing signal, not a branding exercise.

- Focus on assets with water security, solar readiness, and low-density planning because those features improve long-term resilience.

- Use a two-horizon model: lifestyle utility today, intergenerational liquidity tomorrow.

Risk Factors

Regenerative luxury is not immune to macro pressure. India’s premium market can cool if credit tightens, capital gains taxes change, or the rupee weakens against hard-currency comparisons. Some projects market sustainability without delivering operational performance, which creates greenwashing risk. Liquidity is also thinner in bespoke estates than in standard apartments, so exit timing matters. The right conclusion is not to avoid the segment, but to underwrite it more strictly than conventional luxury.

FAQs

What is regenerative luxury real estate?

It is high-end property designed to restore rather than merely reduce harm. That can include native landscaping, water harvesting, renewable energy, low-density planning, and wellness-centered architecture.

Why is India important now?

India’s top-end wealth base is expanding quickly, with HNIs and UHNWIs both rising and office/investment data showing strong capital formation.

Which markets look strongest?

Bengaluru, Delhi-NCR, Mumbai, Hyderabad, Pune, and Goa stand out, with each serving a different wealth motive: income, legacy, privacy, or lifestyle

Is this only for end-users?

No. Many buyers treat premium real estate as capital preservation, family utility, and portfolio diversification at the same time.qa

Conclusion

The next cycle of Indian luxury real estate will not be defined by marble count or headline price per square foot. It will be defined by whether a property can hold wealth, sustain attention, and remain desirable in a more demanding world. Regenerative estates answer that brief with unusual precision: they offer scarcity, beauty, resilience, and a narrative of responsibility that still reads as privilege. For UHNI families, NRIs, and strategic investors, the real opportunity lies in places where land, design, and governance align. That is where new wealth geography becomes durable wealth architecture. Private consultations, curated micro-market notes, and exclusive acquisition reports are now the serious tools of entry.

Free Resources To Download

Beyond Net Zero: Key Points Summary

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post