Now Reading: First-Time Homebuyer in India: What Smart Money Wisely Does Before Signing Anything

- 01

First-Time Homebuyer in India: What Smart Money Wisely Does Before Signing Anything

First-Time Homebuyer in India: What Smart Money Wisely Does Before Signing Anything

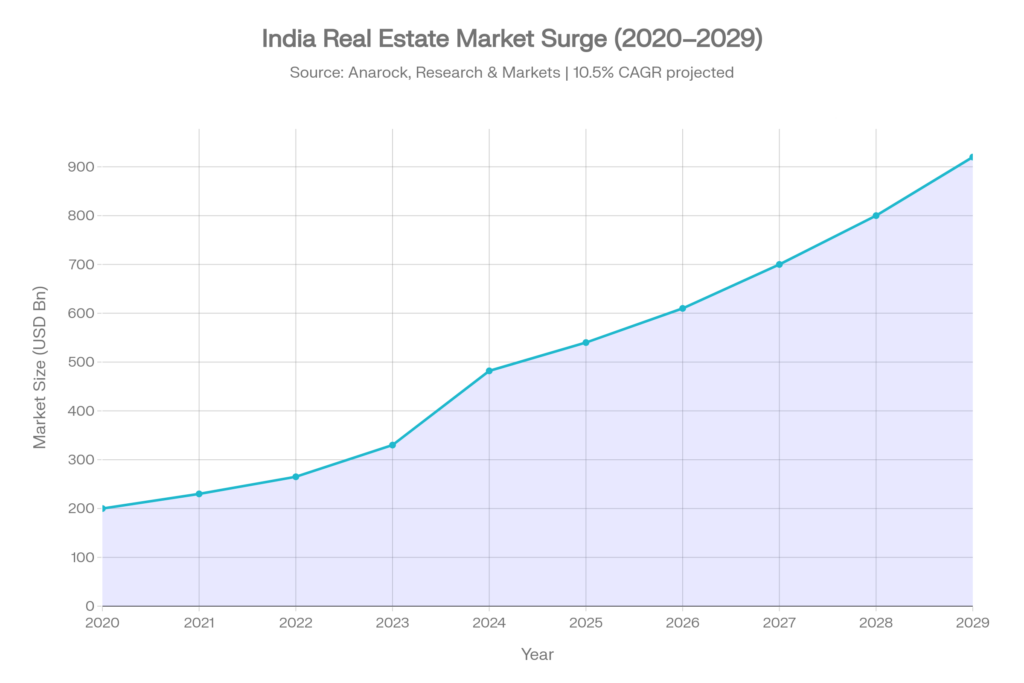

India’s residential real estate market has entered a structural upswing unlike any in the past decade — not a cyclical bounce, but a fundamental repricing of where and how people want to live. The market reached USD 482 billion in 2024 and is projected to grow at a CAGR of 10.5% to USD 1.18 trillion by 2033 . For first time homebuyer, this is both an opportunity and a minefield.

Entry timing matters, but it is secondary to structural decisions: which city, which micro-market, which developer, and how the acquisition is financed. NRI investment surged 20% year-on-year in 2024 to an estimated USD 14–15 billion , signalling that global capital is already running ahead of retail sentiment. First-time buyers who approach this transaction with legal rigour, financial discipline, and market intelligence are positioned not merely to buy a home, but to build lasting wealth in one of the world’s fastest-appreciating asset classes.

Market Shift & Global Context

India’s housing market broke into the global top 10 by price appreciation in 2025, recording 9.6% year-on-year residential price growth according to Knight Frank’s Global House Price Index. That ranking sits alongside markets like Portugal and Australia — economies far older in their property cycles. What makes India’s trajectory unusual is that growth is being led from the top down: luxury units priced above ₹4 crore drove the 2024 surge, not the affordable segment that historically anchored headline numbers.

The global context is instructive. As interest rate cycles in the US and Europe trend downward, institutional capital is rotating toward high-growth emerging markets. India — with a young population, an urbanising middle class, and a regulatory framework reformed by RERA (Real Estate Regulation and Development Act, 2016) — has emerged as the default destination. For the first-time buyer, this convergence of domestic demand and global capital flows means that waiting for prices to correct is not a strategy. It is a gamble against informed institutional consensus.

The critical insight for first-time buyers is segmentation: the affordable housing segment (<₹40 lakh) has seen flat or declining supply as developers pivot to premium and luxury tiers. Buyers in the sub-₹1 crore range face constrained choices and should act with greater urgency than buyers in higher brackets.

Emotional & Lifestyle Drivers

The pandemic reset something fundamental in India’s relationship with property ownership. Post-2020 homebuyers are not simply seeking shelter — they are seeking permanence, autonomy, and a hedge against professional uncertainty. Remote work legitimised suburban and Tier-2 acquisitions; integrated townships in Pune, Hyderabad, and Navi Mumbai surged accordingly.

For NRIs especially, the emotional calculus is layered. Buying in India is, for many, a statement of identity as much as capital allocation — a tethering to family, roots, and the accelerating prosperity of a country in which they see their future. The rupee’s depreciation cycles have historically made Indian real estate even more attractive for dollar- or dirham-denominated earners, creating a recurring buying window that sophisticated NRI investors now model explicitly into acquisition timing.

Case Studies

PMAY Beneficiary: Affordable Segment, Delhi NCR

A 28-year-old first-time buyer in Noida’s Sector 137 secured a 1BHK apartment under PMAY in 2023, availing a credit-linked subsidy of ₹2.67 lakh on a ₹35 lakh home loan. Total effective acquisition cost after subsidy: ₹44.2 lakh for a RERA-registered unit. A six-week legal checklist — encumbrance certificate, mutation records, building plan sanctions — prevented the buyer from proceeding with an alternative project later flagged by UP RERA for completion delays.

Pune First-Time Buyer: Smart Micro-Market Selection

A 32-year-old IT professional in Pune’s Hinjewadi corridor purchased a 2BHK unit in a RERA-registered project in 2022 for ₹68 lakh. By Q1 2025, comparable units in the same project listed at ₹1.05 crore — a 54% appreciation in under three years. The gain was driven by proximity to the proposed Pune Metro Phase 2 corridor, announced six months after purchase. Due diligence on civic infrastructure pipelines — available via PMRDA’s public development plans — was the decisive factor.

NRI Buyer: Bengaluru Luxury Segment

A Dubai-based NRI couple acquired a 3BHK unit in Bengaluru’s Sarjapur Road micro-market in late 2023 for ₹1.8 crore. The transaction was executed entirely remotely via a registered Power of Attorney and RERA-verified documentation. By March 2025, the unit category commanded ₹2.4 crore, with an annual rental yield of approximately 3.2%. The decisive discipline: engaging a RERA-registered broker rather than an unregulated aggregator.

Tips for First-Time Homebuyers

These are not generic advice — they are the exact sequence followed by successful buyers in 2024–2026 transactions, based on checklists from brokers and legal advisors.

Budget Check (Week 1)

Calculate your maximum affordable price: (Annual income × 5) minus existing EMIs. Add 10–15% buffer for stamp duty (5–7% in most states) and registration (1%). Example: ₹15L annual salary → max budget ₹60–70L home. Use online EMI calculators from SBI or HDFC to test at 9% interest over 20 years.

Pre-Approved Loan (Week 2)

Get a home loan pre-approval from 2–3 banks (SBI, HDFC, ICICI). This locks your borrowing power and strengthens your negotiating position with sellers/developers. Required docs: salary slips (3 months), ITR (2 years), bank statements (6 months). NRIs: add passport, visa, and overseas income proof.

Property Shortlist (Weeks 3–4)

Filter RERA-registered projects only, possession within 18–36 months, resale for immediate move-in. Prioritise micro-locations near workplaces/schools (e.g., Whitefield for Bengaluru IT, Dwarka Expressway for Gurgaon commuters). Visit 5–7 shortlisted properties; check for water supply, power backup, and parking.

Legal Due Diligence (Weeks 5–6)

Hire a property lawyer for:

- Encumbrance Certificate (last 13–30 years, from Sub-Registrar).

- Title deed verification (clear chain of ownership).

- Approved building plans (from local municipal corp).

- No Objection Certificates (NOC from society/bank/society).

- RERA project status (rera.gov.in — check complaint history).

- Red flags: Any court cases, disputed land, or unapproved floors.

Negotiation & Agreement (Week 7)

Offer 5–10% below asking price in resale; 3–5% in new launches. Sign Agreement to Sell (10% token payment). Include clauses for possession timeline, penalty for delays (₹5/sq ft/day), and defect liability (12 months post-handover). NRIs: execute via e-stamp and registered PoA.

Full Payment & Registration (Week 8+)

Pay balance via cheque/RTGS (avoid cash >₹2L). At registration: both parties present, pay stamp duty online (e.g., Maharashtra’s e-stamping portal), get mutation updated in revenue records within 30 days. Insure immediately (₹5K–10K/year premium).

Real-World Example: A ₹12L/month-earning Mumbai couple in 2025 shortlisted Thane resale flats (₹1.2Cr budget). They skipped a “bargain” project with 50+ RERA complaints, chose a verified resale with EC clean for 20 years, negotiated ₹8L off, and closed with SBI pre-approved loan at 8.75%. Property appreciated 12% in 6 months.

Risks & Contrarian Perspectives

India’s residential market is not without structural vulnerabilities, and any serious buyer must weigh them:

- Construction and Delivery Risk — Despite RERA’s mandate, project delays remain endemic. Over 4.5 lakh RERA-registered units across India’s top seven cities were classified as delayed by more than 12 months as of 2024 (MahaRERA Annual Report, 2024). Under-construction properties carry delivery risk that resale properties do not.

- Affordability Compression — The luxury segment’s ascendancy has pushed mid-income buyers into increasingly peripheral micro-markets. When commute times exceed 60 minutes and social infrastructure remains underdeveloped, resale liquidity in those pockets is structurally limited.

- Interest Rate Sensitivity — India’s home loan book grew 58% between 2022 and 2024, much of it at floating rates. A sustained rate elevation cycle could materially affect EMI affordability across the ₹40L–₹1.5 crore segment, where leveraged demand is highest.

- Regulatory Opacity in the Resale Market — RERA governs new launches but offers limited protection in the secondary/resale market. Title disputes, undisclosed encumbrances, and illegal construction regularisation remain common. Independent legal due diligence is not optional.

- Geographic Concentration Risk for NRIs — NRI investors tend to cluster in Bengaluru, Pune, and Hyderabad — markets already at elevated valuations. Concentration in a single city without micro-market diversification amplifies downside in a correction scenario.

FAQs

What is the most important legal document to verify when buying a first home in India?

The Encumbrance Certificate (EC) is the single most critical document — it confirms the property carries no outstanding loans, legal disputes, or financial liabilities. Complement it with a verified title deed tracing ownership for 30 years, a current tax receipt, and RERA registration confirmation. A property lawyer’s title opinion is a worthwhile investment.

Can NRIs buy residential property in India, and what are the restrictions?

Yes — NRIs and Persons of Indian Origin (PIOs) can purchase residential and commercial property in India under FEMA without RBI approval. They cannot purchase agricultural land, plantation property, or farmhouses without specific government clearance. Home loans are available via Indian banks’ NRI divisions, and funds must be routed through NRE/NRO accounts.

What is a sustainable home loan EMI-to-income ratio for a first-time buyer?

Total EMI obligations should not exceed 40–45% of gross monthly income. For a buyer earning ₹1.5 lakh/month, a safe EMI ceiling is approximately ₹55,000–₹60,000 — corresponding to a loan of roughly ₹55–60 lakh at current rates of 8.5–9%.

Conclusion

India’s property market is not a monolith — it is a mosaic of micro-markets, each with distinct supply dynamics, infrastructure trajectories, and buyer profiles. For first-time homebuyers, the decisive advantage is not capital, but intelligence: knowing which documents to demand, which infrastructure projects to track, and which developer track records to interrogate. The structural tailwinds — demographic expansion, rising household incomes, and institutional capital inflows — will not wait for the unprepared.

The next three years will likely see continued appreciation in Tier-1 micro-markets and a gradual maturation of Tier-2 cities as genuine alternatives. Buyers who act with rigour now, rather than waiting for an imagined correction, will likely look back at this window as the defining wealth-creation decision of their generation. For personalised guidance — whether in Mumbai, Bengaluru, or from Dubai — consult a RERA-registered advisor or seek an independent legal opinion before any commitment. Your first home should be the foundation of a portfolio, not an impulsive transaction.

YouTube Resources

Free Resources To Download

First-Time Homebuyer India: Key points summary