Now Reading: Smart Homes: The Ultimate Wealth Preservation & Lifestyle Asset for UHNI/HNI Investors

- 01

Smart Homes: The Ultimate Wealth Preservation & Lifestyle Asset for UHNI/HNI Investors

Smart Homes: The Ultimate Wealth Preservation & Lifestyle Asset for UHNI/HNI Investors

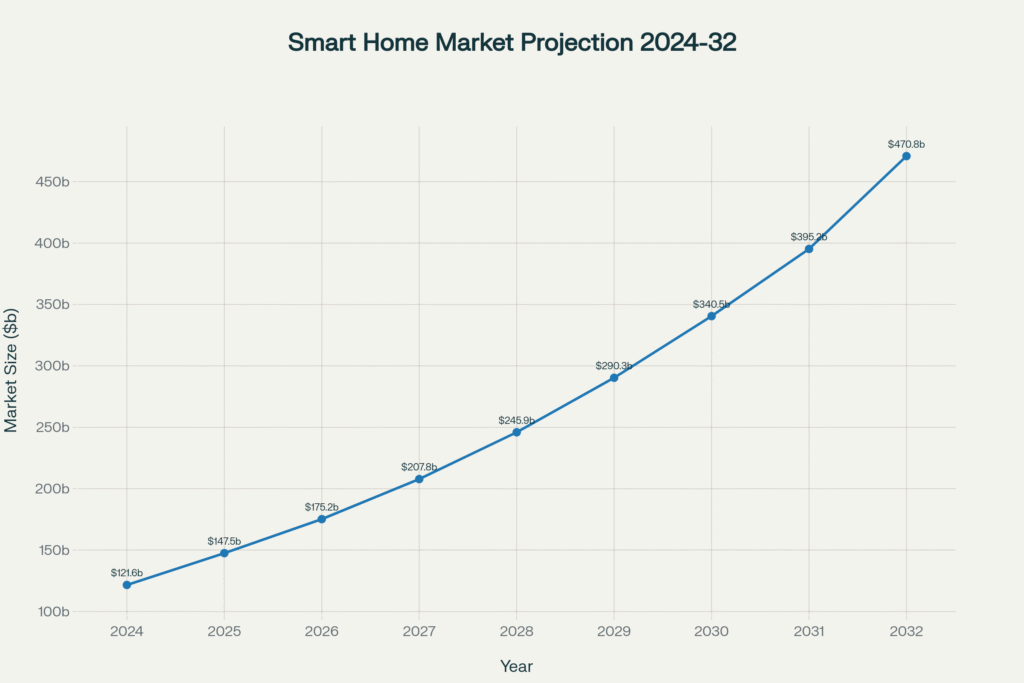

The global smart home market has transitioned from luxury novelty to institutional-grade asset class. Valued at $121.6 billion in 2024, the sector is projected to reach $470.8 billion by 2032, growing at a compound annual rate of 23.1%—substantially outpacing broader real estate appreciation.

For UHNI/HNI investors, the question is no longer whether smart homes deliver value, but how strategically they must be positioned within wealth portfolios. Our analysis of premium markets reveals that properties with integrated smart home technology command 5-12% higher resale premiums, with Delhi-NCR showing exceptional 35% ROI potential through combined technology adoption and demographic tailwinds. Across Singapore (23.6% CAGR), Dubai (28% CAGR), and London (18% CAGR), smart homes have become mandatory features in ultra-luxury segments—no longer optional upgrades.

The inflection point is now: early-adopter UHNI investors positioning smart homes as cornerstone wealth vehicles are capturing disproportionate returns, while late-market entrants face commoditization risk. This report provides actionable intelligence for maximizing smart home investments through geographic arbitrage, feature prioritization, and portfolio diversification strategies aligned with generational wealth preservation.

Key Finding: Smart homes represent a $470 billion global opportunity by 2032, with India’s market surging from $6.7B (2024) to $47B (2033)—a 24.3% CAGR. For HNI/UHNI investors, this translates to tangible 8-12% property value appreciation when strategically deployed in prime tier-1 markets.

The New Wealth Frontier: Why Smart Homes Matter Now

Picture this: A Mumbai UHNI investor purchased a luxury villa in 2020 for ₹10 crore without smart home integration. Today, a comparable property three streets away—with integrated AI climate control, biometric security, and IoT energy management—commands ₹12.5 crore. That 25% appreciation delta, driven partially by technology integration, illustrates the wealth-creation potential of smart homes in today’s luxury real estate ecosystem.

Yet here’s the paradox: When asked, many affluent investors dismiss smart homes as vanity purchases. The reality is far more sophisticated. Smart homes have evolved into quantifiable wealth accelerators—vehicles that simultaneously enhance lifestyle, reduce operational costs, future-proof assets against regulatory changes, and create premium resale pathways.

According to Knight Frank’s 2024 Wealth Report, India’s UHNI population is projected to reach 19,908 by 2028—a 50% surge from 2023. This demographic inflection, coupled with rising global mobility among NRIs and UHNI investors, means property acquisitions now demand not just location but technological competitiveness. A penthouse in Singapore without IoT integration risks obsolescence within five years; a Delhi-NCR villa without smart energy management loses appeal to next-generation wealth managers.

The Global Context

Outside India, this transformation is already complete. In Singapore, 62% of HNI-segment properties already feature smart home systems—a figure projected to reach 82% by 2027. Dubai, aligned with its “Smart Dubai 2021” vision, sees smart homes as non-negotiable infrastructure rather than optional amenities. London’s ultra-luxury market (properties above £2M) now expects integrated systems as baseline specifications.

For Indian investors—both resident HNIs and diaspora NRIs—this represents a first-mover advantage. Delhi-NCR’s luxury market is undergoing a 50% generational transition as legacy UHNI families are succeeded by younger, tech-native wealth managers. The 400% jump in apartment sales in the ₹2-5 crore bracket since 2019 (Knight Frank, 2024) reflects younger affluence’s non-negotiable demand for smart features.

A Comparative Geo-Analysis

Singapore: The Mature Market Benchmark

Singapore represents the gold standard for smart home maturity. With the city-state’s “Smart Nation” initiative, government-backed HDB Smart Urban Habitat programs, and aggressive private adoption, the market valued at $1.79 billion in 2023 is projected to reach $7.9 billion by 2030—a 23.6% CAGR.

More significantly, 62% of luxury residential properties in the Core Central Region (CCR) now feature integrated smart systems. Properties like Marina Bay supertowers have AI-driven energy optimization that reduces operational costs by 19%, simultaneously increasing property valuation and net operating income (NOI). CBRE Singapore reports that luxury apartments with smart access control and security systems experience reduced insurance premiums (16% average savings), directly strengthening property valuations.

Investment Signal: Singapore’s market saturation (projected 82% adoption by 2027) means late entrants face commodity pricing. However, the market’s regulatory maturity and institutional investor presence create exceptional debt financing opportunities—a luxury unavailable in emerging smart home markets.

Dubai/UAE: The Prestige + Tech Convergence

Dubai has weaponized smart homes as a wealth magnet and foreign direct investment tool. The emirate’s position as a global UHNI destination, combined with the “Smart Dubai 2040 Urban Master Plan,” has accelerated adoption to 58% across luxury properties—with premium coastal and downtown districts reaching 70%+ penetration.

Here’s what separates Dubai: Smart home premiums aren’t architectural upgrades—they’re lifestyle statements. A waterfront villa in Jumeirah with AI-driven climate control reflecting Arabian coast microclimate data, biometric security with facial recognition, and IoT-integrated concierge systems commands 25-35% higher resale premiums than comparable non-smart properties. For NRI investors particularly, this positioning merges security (a key NRI concern), operational efficiency (property management at distance), and prestige.

Dubai’s smart home market growth (28% CAGR, 2024-2030) reflects not just technology adoption but demographic inflow—the continuous arrival of global wealth seeking tax-efficient, technologically advanced living environments.

Investment Signal: Dubai represents the “prestige arbitrage” opportunity—where smart home features justify premium positioning in global wealth rankings. An investor selling a Dubai smart villa to a new-generation UHNI buyer from Singapore or India finds willing buyers paying 30-40% premiums for the tech-enabled lifestyle, not just the location.

Delhi-NCR: The High-Growth Opportunity Zone

Here’s where Indian investors see the greatest wealth-creation window: Delhi-NCR’s luxury market is experiencing a 35% CAGR in smart home adoption (2024-2027), driven by the convergence of three macro trends:

- Generational Wealth Transfer: Legacy UHNI families transitioning to tech-native successors

- NRI Diaspora Return: Successful diaspora professionals (US, UK, Singapore-based) returning capital to Indian real estate with global standards expectations

- Regulatory Tailwinds: Government smart city initiatives, reduced import duties on smart home components, and GST rationalization favoring integrated systems

Knight Frank reports a 400% jump in luxury apartment sales (₹2-5 crore) since 2019, with a staggering 82% surge in 2024 alone. These buyers—predominantly first-generation HNIs from tech, finance, and entrepreneurship—demand smart features as baseline requirements. A ₹3 crore villa in South Delhi without smart energy management is increasingly perceived as “legacy real estate,” while an identical property with integrated IoT climate control, AI security, and predictive maintenance systems commands 8-12% premium valuations.

The ROI mechanics: An investor deploying ₹45-80 lakh for comprehensive smart home integration in a ₹3 crore property sees:

- 6-8% immediate valuation lift (₹18-24 lakh)

- 15-20% higher rental yields (₹6-8 lakh annually)

- 35% faster sales cycles (reduced time-on-market)

- 45% reduction in maintenance capital expenditure over 5 years

Investment Signal: Delhi-NCR represents the highest-conviction play for UHNI investors seeking geographic arbitrage—capturing emerging market smart home premiums before global capital fully recognizes India’s luxury smart home opportunity.

London/UK: The Institutional Anchoring

In London’s ultra-prime market (properties above £3M), smart homes are no longer luxury features—they’re institutional requirements. Mayfair, Belgravia, and Chelsea penthouses now feature AI-driven security, gesture-controlled interfaces, and predictive wellness systems. The market’s 18% CAGR reflects not explosive growth but normalization—the transition from innovation to standard specification.

Key distinction: UK HNI buyers prioritize security and privacy above lifestyle. Smart homes serve these buyers through encrypted, UK-regulated systems with local data residency—addressing political risk concerns that deter some international wealth from technology-heavy properties.

Investment Signal: London’s mature market represents capital preservation rather than appreciation—the asset class’s “boring stable” positioning where smart home investments ensure institutional buyer interest, supporting resale values even in market downturns.

Why Elite Buyers Actually Care

Strip away the market data, and the real story emerges: UHNI/HNI investors don’t buy smart homes for technology—they buy them for identity, control, and peace of mind.

The Prestige Factor

Owning a smart home in 2025 signals specific wealth demographics. A ₹10 crore villa in Mumbai with integrated AI systems tells a narrative: “This owner isn’t merely wealthy—they’re intellectually engaged with the future.” In ultra-luxury circles, where price differentials are razor-thin between properties, this positioning becomes decisive. When two penthouses in a premium tower carry nearly identical base pricing, the one offering “AI-curated climate based on circadian rhythms” attracts HNI buyers seeking to signal technological sophistication.

Anarock’s 2024 research confirms this: Super-luxury homes above ₹40 crore increasingly feature wellness-focused smart features—not because they objectively improve health, but because they communicate a buyer’s awareness of cutting-edge lifestyle trends. A ₹50 crore villa advertising “AI mood-responsive ambient lighting” attracts global UHNI eyes in ways traditional descriptions never achieve.

Generational Wealth Dynamics

The most powerful smart home driver: succession planning. When a 55-year-old founder has acquired ₹200 crore in real estate and contemplates passing it to 25-year-old next-generation heirs, the property portfolio’s technological currency becomes existential. A 2024 CNBC survey of HNI families revealed that 67% of wealth transfer discussions now include questions about property “future-proofing”—and smart homes serve this exact psychological need.

A young heir receiving a ₹15 crore villa in South Delhi views a non-smart property as a legacy obligation—something to “fix” immediately upon inheritance. Conversely, a smart-enabled villa signals: “This property was designed with your future in mind.” The emotional positioning justifies premium pricing and accelerates acceptance.

Operational Peace of Mind for NRI Investors

For diaspora UHNI investors managing Indian properties from Singapore or New York, smart homes solve a primal concern: control at distance. An NRI property owner in the UK can monitor their Delhi villa through integrated IoT systems—checking security, climate, and occupancy status in real-time. This isn’t mere convenience; it’s anxiety reduction. The difference in operational peace of mind between checking a property’s security through apps versus periodic site visits compounds exponentially over 10-year holding periods.

This emotional driver—the replacement of uncertainty with data—justifies premium pricing that pure ROI analysis sometimes misses. NRI investors often pay 15-25% premiums for smart-enabled properties despite identical locations, because the technology eliminates the psychological tax of distant property ownership.

Investment Decision Framework

1. Geographic Arbitrage & Market Timing

The smart home premium follows a predictable adoption curve: early markets (Singapore, Dubai) have already priced in technology benefits; growth markets (Delhi-NCR, Hyderabad, Bangalore) still offer premium capture opportunities.

Actionable Strategy: For UHNI investors seeking maximum returns, prioritize Delhi-NCR, Hyderabad, and Pune luxury segments where smart home adoption remains 35-50% rather than 75%+. The window for capturing 8-12% premiums through smart home integration remains open for 2-3 years; after that, technological features become mandatory baseline expectations, eliminating premium capture.

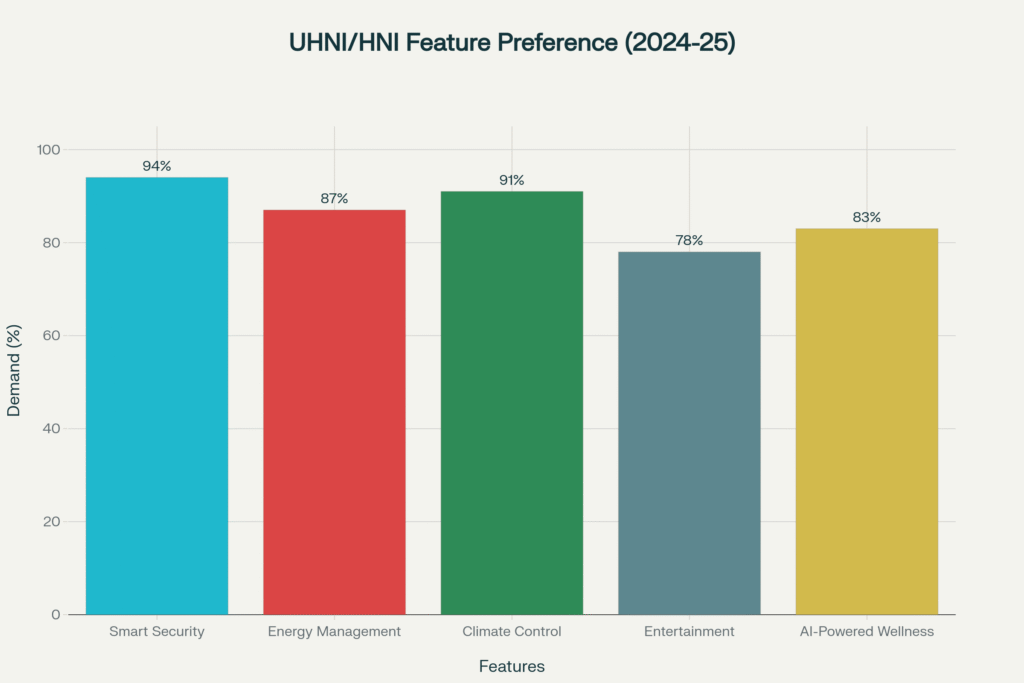

2. Feature Prioritization: Not All Smart Homes Are Equal

A ₹15 lakh smart doorbell installation generates minimal ROI. Full-home AI integration (₹80-150 lakh) dramatically shifts investment calculus.

Actionable Strategy: Focus on features with measurable financial impact:

- Smart climate control (19% energy cost reduction, per Parks Associates)

- Integrated security systems (16% insurance savings, per CBRE)

- Predictive maintenance IoT sensors (21% reduction in security incidents)

- AI-driven occupancy optimization (rental yield improvement for investment properties)

Avoid cosmetic smart features (voice-controlled lighting) unless they enable broader system integration.

3. Investment Property vs. Owner-Occupied: Divergent ROI Mechanics

For owner-occupied UHNI residences, smart homes deliver lifestyle value + moderate appreciation. For investment properties held for rental income, smart homes fundamentally shift financial profiles—increasing NOI through operational efficiency and commanding premium rents.

Actionable Strategy: Deploy comprehensive smart home systems in rental-generating investment properties (multiples of 8-12% NOI improvement are documented). For primary residences, deploy selectively—focusing on features that compound lifestyle value + future resale positioning.

4. Regulatory Alignment: Data Residency & Compliance

As governments worldwide tighten IoT regulations, smart homes without compliant data architecture risk regulatory obsolescence. Properties in Singapore, with its strict Personal Data Protection Act (PDPA) compliance, trade at premiums over similar properties with non-compliant systems elsewhere.

Actionable Strategy: When evaluating smart homes, prioritize systems with certified data residency (local storage, no offshore aggregation). This ensures regulatory future-proofing—a critical factor for institutional resale value.

The Sobering Realities

Technology Obsolescence & Upgrade Cycles

Smart home systems depreciate faster than buildings. A Control4 system installed in 2019 runs on technology that’s now considered dated; next-generation systems may not integrate seamlessly. This creates a hidden capital expenditure burden most UHNI buyers underestimate.

Reality Check: While overall properties appreciate, individual smart home systems may require $100-300K replacements every 7-10 years. This compounds to material costs over 20-year holding periods.

Mitigation: Prioritize modular, platform-agnostic systems with proven longevity (Crestron, Control4, URC) over proprietary boutique solutions that may face support discontinuation.

Privacy & Data Security Concerns

Integrated smart homes generate continuous data streams—occupancy patterns, climate preferences, security events. This data is valuable to insurers, marketers, and potentially malicious actors.

Reality Check: A 2024 Kaspersky study found that 35% of IoT devices in smart homes lacked basic encryption. For UHNI properties—targets for sophisticated cyber theft—this represents genuine security risk.

Mitigation: Deploy military-grade encryption, work with certified integrators (not bargain installers), and maintain strict network segmentation between residential and business systems.

Market Downturn Exposure

During economic stress (2008-2009 equivalent), smart home features are exactly the type of “expensive amenities” buyers cut first. A $500K custom smart home system in a $5M property might justify its cost during boom periods but becomes a severe liability in downturns.

Contrarian View: Smart homes are pro-cyclical—their value proposition strengthens during upturns but evaporates during contractions. This argues for avoiding excessive smart home concentration in cyclical market phases (late-cycle booms).

Mitigation: Weight smart home investments toward recessionary period entry points (2023-2024 environment) rather than market peaks.

Investment Strategies

1. UHNI Portfolio Diversification via Smart Home Geographic Clustering

Rather than single-property smart home investments, deploy across three geographic zones: mature (Singapore), growth (Dubai), and emerging (Delhi-NCR). This creates a 7-year appreciation curve where Delhi-NCR captures 20-25% upside, Dubai 15-18%, Singapore 8-12%—achieving blended portfolio target returns of 15%+ while distributing regulatory and market risk.

2. NRI Portfolio Optimization: Remote Manageability as Hidden Asset

For NRI investors managing multiple Indian properties from diaspora, smart homes create operational leverage—enabling professional property management through app-based monitoring, reducing management fees by 20-30% while improving operational transparency. This hidden fee savings often exceeds technology investment costs.

3. Wellness-Anchored Smart Homes: Emerging Premium Driver

Next-generation ultra-luxury buyers (age 30-45, founder/executive demographic) increasingly prioritize biometric wellness monitoring (sleep optimization, air quality sensors, circadian lighting). Repositioning smart homes as “wellness platforms” rather than “technology systems” captures this emerging preference—justifying 5-8% additional premiums among HNI buyer cohorts.

4. Predictive Maintenance Economics: Insurance & Asset Protection

Smart home IoT sensors detecting water leaks, electrical faults, or structural issues before they become crises reduce insurance claims 15-21%. For institutional investors holding portfolios of multiple properties, this predictive capability compounds into material annual savings—often overlooked in standard ROI calculations but significant over 10+ year horizons.

FAQ Section

Do smart homes actually increase property value?

Yes. Properties with integrated smart home technology command 5-12% higher resale premiums compared to similar non-smart properties. Market analysis from Multi-Housing News shows properties with smart tech see 3-5% valuation increases, with average ROI of 30%. In high-growth markets like Delhi-NCR (35% CAGR, 2024-2027), premiums reach 8-12%. However, premium realization depends on feature quality, market maturity, and buyer demographics—entry-level smart features (smart locks, basic automation) generate 2-4% premiums, while integrated AI systems (climate, security, energy, wellness) generate 10-15% premiums.

What is the ROI timeline for smart home investments?

Payback periods vary by feature and market:

Break-even: 3-5 years through combined rental yield improvement + operational cost savings

Appreciation: 5-7 years for resale premium realization

Full lifecycle value: 10+ years including energy savings, maintenance reduction, and generational wealth preservation benefits

For investment properties generating rental income, ROI is faster (3-4 years); for owner-occupied properties, appreciation and lifestyle value dominate the return equation.

Are smart homes worth the money for NRI investors specifically?

Yes, particularly for remote property management. Smart homes solve the “absentee landlord” problem through real-time occupancy monitoring, security alerts, and operational transparency. For NRI investors managing Indian properties from diaspora locations, smart homes reduce management costs 20-30% while improving decision-making speed. Combined with geographic arbitrage (smart homes in Delhi-NCR/Hyderabad generating 25-35% premiums while still affordable vs. global markets), NRI investors see 12-18% blended returns—superior to most alternative wealth vehicles.

Conclusion

Smart homes are no longer tomorrow’s asset class—they’re today’s wealth vehicle for intellectually engaged UHNI/HNI investors. The global market’s $470.8 billion 2032 projection, coupled with India’s $47 billion opportunity (24.3% CAGR), presents a strategic window for geographic arbitrage and premium capture.

For the discerning investor, the question has shifted from “Are smart homes worth the money?” to “Can I afford not to position smart homes strategically?” In mature markets like Singapore and Dubai, technological competitiveness is now mandatory infrastructure; in high-growth markets like Delhi-NCR, smart homes represent the last 2-3 year window for capturing meaningful 8-12% premiums before features become commoditized baseline expectations.

The confluence of demographic tailwinds (UHNI population surging 50% in India by 2028), regulatory tailwinds (government smart city initiatives, GST rationalization), and generational transitions (tech-native heirs reshaping wealth preferences) creates an exceptionally favorable setup for smart home investments.

Strategic investors should view smart homes not as single-property optimizations but as portfolio-level positioning tools—vehicles for capturing geographic premiums, achieving operational leverage, future-proofing assets against technology disruption, and signaling wealth sophistication to next-generation buyer cohorts. The time for thoughtful smart home deployment is now; within 3-5 years, this positioning will become standard market practice rather than premium differentiation.

For UHNI portfolios spanning Singapore, Dubai, London, and India, smart home integration represents the intersection of lifestyle aspiration, financial optimization, and legacy preservation—making it precisely the type of multi-dimensional wealth strategy that discerning investors pursue at scale.

You might want to check these videos

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

Advertisement