Now Reading: Luxury Residences in India: A Strategic Asset Class for Global Wealth

- 01

Luxury Residences in India: A Strategic Asset Class for Global Wealth

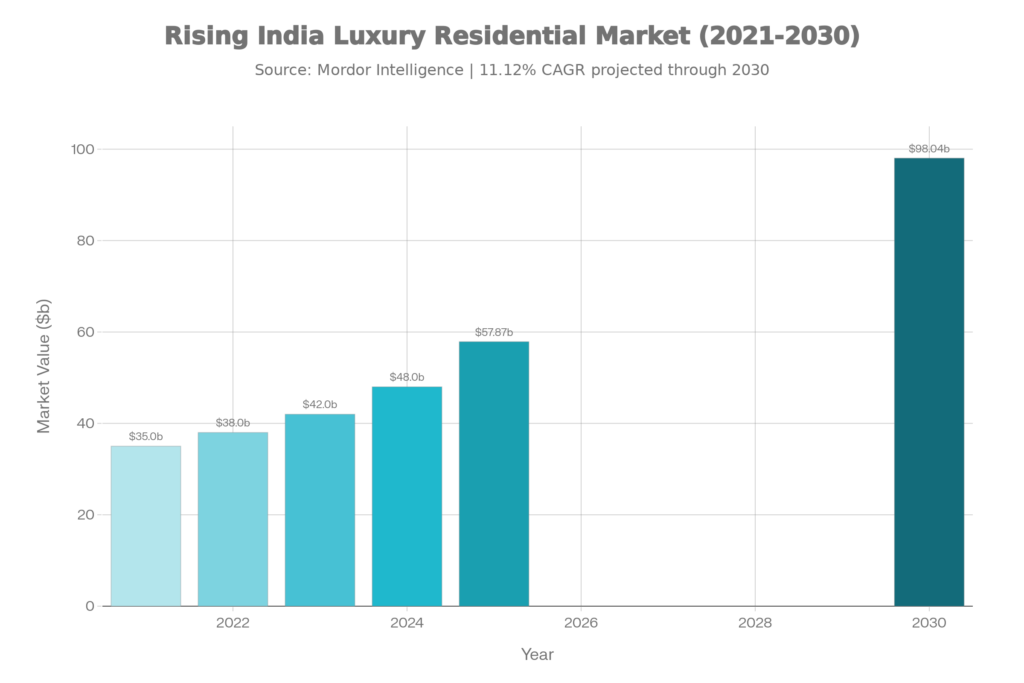

India’s market for luxury residences has crossed a structural inflection point. Valued at USD 57.87 billion in 2025 and projected to reach USD 98.04 billion by 2030 at an 11.12% compound annual growth rate (CAGR), the segment is no longer niche—it is the dominant narrative of the nation’s real estate evolution. The first half of 2025 witnessed homes priced above ₹1 crore accounting for nearly 50% of total residential sales, a seismic shift from mid-range housing. What began as aspirational wealth preservation has crystallized into institutional confidence: ultra-high-net-worth individuals (UHNI), high-net-worth individuals (HNI), and global NRI investors are deploying capital across Mumbai, Delhi-NCR, Bengaluru, and emerging markets like Hyderabad with conviction typically reserved for publicly listed equities.

This is not speculative appetite. This is strategic capital allocation into hard assets offering 8–12% annual appreciation, low vacancy rates (under 5%), and rental yields of 3.5–4% in prime markets—significantly outperforming conventional mid-range residential. The exclusivity, however, commands discipline: location specificity, developer pedigree, and sustainability credentials have become non-negotiable filters for discerning investors navigating India’s premiumized residential landscape.

The Transformation and Context

The structural realignment of India’s residential market mirrors the wealth expansion dynamics unfolding across South Asia. The country now hosts nearly 86,000 ultra-rich individuals—a cohort expanding at 6.1% annually and projected to exceed 19,900 UHNI households by 2028. This affluence, concentrated in financial services, technology, entrepreneurship, and professional sectors, has created an insatiable appetite for trophy assets that transcend functional housing.

Mumbai, the financial epicenter, has witnessed median luxury apartment prices climb to ₹9.66 crore (approximately USD 1.16 million), while Delhi-NCR’s Golf Course Road transactions command ₹15 crore and beyond. Yet the market’s most compelling narrative is not concentration but geographic dispersion.

Bengaluru, traditionally a mid-income stronghold, now registers 48% year-on-year growth in luxury segment sales—catalyzed by the region’s emergence as a global technology hub and the flight of venture capital into tangible assets. Hyderabad, meanwhile, posts a blistering 13.12% CAGR, driven by infrastructure modernization (airport corridor expansions) and a rising cohort of technology-sector entrepreneurs seeking lifestyle upgrades beyond conventional rental markets.

This premiumization reflects a deeper global phenomenon. As international capital encounters regulatory friction and geopolitical uncertainty, India’s luxury real estate has acquired credibility as a stable, transparent, and appreciating asset class. The rupee’s weakness against the US dollar has fortified the appeal for NRI investors deploying foreign earnings back into India—a constituency that contributed 20% of luxury segment investments in 2024, a 12% increase year-on-year.

Market Analysis & Performance Indicators

Market Scale and Growth Trajectory

The luxury residential sector (units priced at ₹4 crore and above) recorded a 37.8% year-on-year increase in sales during the first nine months of 2024, translating to 9,685 units transacted across major cities. The first half of 2025 accelerated this momentum, with total luxury housing sales exceeding 11,400 units—an 82% year-on-year surge recorded between July and September 2025. Current market valuation stands at ₹4,83,000 crore (approximately USD 57.87 billion at current exchange rates), positioning India’s luxury segment as one of Asia’s fastest-growing residential markets by percentage growth, though still modest relative to China and Hong Kong in absolute terms.

City-Wise Concentration and Leadership

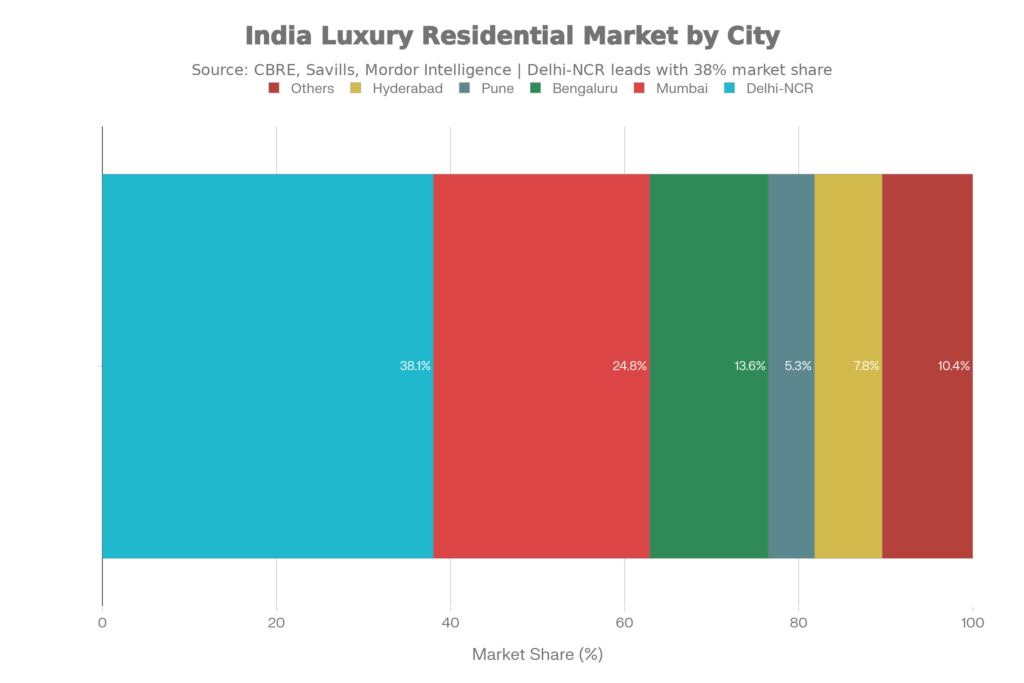

Delhi-NCR dominated H1 2025 with 5,855 luxury unit sales—a 72% year-on-year increase—accounting for 49% of national luxury sales. The region’s momentum is anchored by institutional supply: 6,100 new luxury units launched in H1 2024, with developers capitalizing on abundant land parcels and expressway connectivity to position large-format gated enclaves. Mumbai maintained a 33% national share (3,820 units sold, 18% YoY growth) but retained the highest price ceiling: average transaction values in South and Central Mumbai exceed ₹8–10 crore, underscored by limited coastline availability and heritage location premiums.

Bengaluru’s ascent is undeniable. The city logged 48% year-on-year growth in luxury sales and saw average capital values in under-construction projects surge 32–35% YoY, with Central Bengaluru recording the sharpest appreciation of 45–48% YoY. Pune entered the top-tier conversation with 810 luxury unit sales in H1 2025—an 18% growth rate reflecting corporate migration from metros and lifestyle arbitrage attracting affluent buyers.

Price Dynamics and Appreciation Patterns

Average luxury apartment prices across major metros appreciated from ₹14,530 per square foot in 2022 to ₹20,300 per square foot by 2025—a 39.8% cumulative increase over three years. Yet appreciation velocity is asymmetric: under-construction luxury properties in Mumbai surged 44% year-on-year in H1 2025, while completed high-end stock appreciated 1% YoY, reflecting developer pricing power on new launches and buyer preference for modern specifications (open layouts, Vaastu orientation, proximity to the Coastal Road).

Bengaluru’s under-construction segment outpaced completed inventory appreciation, mirroring a supply-demand inversion where limited prime land scarcity inflates developer pricing for early-stage projects. Delhi-NCR’s luxury market exhibited more temperate dynamics: Golf Course Road recorded 21% and 33% appreciation for completed and under-construction apartments respectively, while South East Delhi plots appreciated 15% YoY, signaling selective hotspots rather than blanket market gains.

Rental Markets: Yield and Tenant Demand

India’s luxury apartment rental segment has emerged as a parallel growth engine. Average rental yields for luxury apartments range from 3.5% to 4% annually—significantly outperforming mid-range residential at 2–2.5%—with vacancy rates under 5% compared to over 10% for standard housing. Central Bengaluru’s rental market recorded a sharp 40–45% year-on-year spike in average rents for H1 2025, driven by corporate mobility from Tier-2 cities and expat inflows to technology campuses.

Mumbai’s premium rental segment surged 2–17% YoY, propelled by end-user preference for spacious, low-density residences offering privacy and sea views. Delhi witnessed a 34% year-on-year increase in rental values, with South West and South East micromarkets recording 42% and 35% appreciation respectively—reflecting diplomat and expatriate demand for gated, amenity-rich residences.

Branded Residences: The Global Luxury Inflection

The fastest-growing luxury subsegment is branded residences—residential developments co-developed with global luxury hospitality and lifestyle brands. India has ascended to sixth position globally for live branded residence projects (Knight Frank, 2025), contributing 4% to worldwide supply and ranking 10th in pipeline projects representing 2% of future global supply. This ranking reflects the presence of Four Seasons, Ritz-Carlton, Mandarin Oriental, Armani, Bentley, and Aston Martin residences across Mumbai, Delhi-NCR, Bengaluru, and emerging markets like Goa.

The segment appeals to globally mobile Indian executives accustomed to international standards and seeking concierge services, wellness pavilions, and IGBC Platinum sustainability certifications integrated into residential fabric. Average transaction values for branded residences command a 15–25% premium over comparable non-branded luxury apartments, justified by operational quality, brand equity, and amenity curation.

Psychological Imperatives & Lifestyle Positioning

Beyond financial metrics, India’s luxury apartment market is propelled by psychological imperatives often invisible to quantitative analysis. For the globally mobile professional—the executive who has lived in London, Dubai, or Singapore—India’s luxury residences represent cultural homecoming married with international standards. This buyer seeks not mere opulence but experiential integrity: architectural coherence, service excellence, wellness integration, and environmental stewardship. The pandemic’s aftermath accelerated this psychological shift. As remote work enabled geographic flexibility, affluent professionals reconsidered India not as a place to “return to” but as a lifestyle destination offering heritage, weather, professional ecosystems, and social capital unavailable in the West.

Lifestyle drivers are multifaceted. Wellness amenities—private spas, yoga studios, salt-water pools designed for recovery—reflect the buyer’s holistic health philosophy. Sustainability credentials (IGBC Platinum, LEED certification) signal alignment with global environmental consciousness. Concierge services, private elevator access, and customizable interiors cater to privacy imperatives acute in India’s scrutinized wealth landscape. The aspirational buyer is drawn to communities, not just residences: curated social environments where professional networks intersect with leisure pursuits. Branded residences, in this context, function as social anchors—Four Seasons residents attend curated events, networking forums, and experiences that extend beyond property boundaries into lifestyle membership.

Heritage and place are potent emotional drivers. A sea-view penthouse in South Mumbai doesn’t just offer real estate appreciation; it confers belonging to a geographic elite whose neighbors include industrial magnates, film personalities, and publishing leaders. Similarly, a luxury villa in suburban Mumbai’s Lodha Codename (a gated ultra-luxury enclave) signals arrival into a new class of residential privilege. For NRI investors, the emotional driver is intergenerational: a trophy property in India functions as cultural anchor, legacy wealth preservation, and a tangible asset their children can inherit or occupy during extended stays, reconnecting them with heritage.

City-Wise Luxury Market Dominance

| City | YoY Growth (%) | Market Share (%) | Key Growth Driver |

|---|---|---|---|

| Delhi-NCR | 72% | 49% | Expressway connectivity, supply availability |

| Mumbai | 18% | 33% | Coastline scarcity, financial sector wealth |

| Bengaluru | 48% | 18% | Tech sector migration, infrastructure upgrades |

| Pune | 18% | 7% | Corporate relocation, lifestyle arbitrage |

| Hyderabad | 13.12% CAGR | 10% | Tech hub emergence, airport corridor |

| Others | 12% | 13% | Emerging second-home destinations (Goa) |

Source: CBRE H1 2025, Savills India, Mordor Intelligence

Vulnerability Factors

Supply-Demand Inversion Risk

While current demand metrics appear robust, the market risks oversupply if 6,100+ new luxury units launched in Delhi-NCR annually exceed absorption rates. High-rise luxury apartments in major metros face density saturation; future growth may be constrained by land scarcity unless developers pivot toward lower-density communities. Price sustainability in secondary markets (Pune, Hyderabad) depends on corporate employment growth; a technology sector slowdown would materially impact asset appreciation.

Regulatory and Tax Uncertainty

India’s tax treatment of real estate income—including the distinction between self-occupied and investment properties, GST implications, and potential capital gains tax indexation changes—remains a policy variable that could compress yields. Proposed residential property wealth taxes (presently under government consideration in select states) could disproportionately impact UHNI portfolios. Currency depreciation also affects NRI investor returns; rupee weakness is currently a tailwind for dollar-earning investors, but future appreciation would reverse this advantage.

Geopolitical Capital Flow Restrictions

Increased scrutiny of foreign direct investment, particularly from Middle East and South Asian sources, could restrict NRI capital inflows that currently represent 20% of luxury segment investments. Economic sanctions regimes (Russia, Iran) have historically redirected capital flows; future geopolitical fragmentation could reduce international demand for India’s trophy assets.

Contrarian View: Premiumization May Mask Wealth Stagnation in Mid-Income Segments

The celebrated shift toward luxury residential investment reflects not broad-based wealth creation but concentration of gains within UHNI/HNI cohorts. Mid-income housing affordability has deteriorated; projects below ₹1 crore are structurally challenged by input cost inflation and construction finance constraints. This wealth polarization, while beneficial for luxury asset appreciation, carries long-term social and macroeconomic risks if unaddressed by policy intervention.

FAQ Section

What is the current average price of luxury apartments in India’s top markets?

Average luxury apartment prices vary significantly by city. Mumbai commands upwards of ₹10 crore in South/Central zones. Delhi-NCR ranges ₹7–75 crore in premium locales like Lutyens Zone and Golf Course Road. Bengaluru spans ₹3–7 crore, with Central Bengaluru (CBD) commanding premiums exceeding ₹5–6 crore. Pune ranges ₹2.5–5.5 crore, making it the most accessible metro-luxury market. Hyderabad is priced ₹2–6 crore, offering favorable entry points for early-stage investors[Source: CBRE H1 2025, Savills India].

What rental yield can I expect from luxury apartment investments in India?

Luxury apartment rental yields range 3.5–4% in established markets (Mumbai, Delhi-NCR) but reach 8–10% in emerging markets (Bengaluru CBD, Hyderabad). Central Bengaluru currently offers the highest yields at 9.9% gross on completed projects, while rental premiums in luxury branded residences (Four Seasons, Ritz-Carlton) reach 4.1–4.3% due to brand-enhanced occupancy rates. Vacancy rates under 5% in luxury segments significantly outperform mid-range residential at over 10%[Source: Shubhashish Homes Research, Savills H1 2025].

Are branded residences worth the premium in India?

Yes, branded residences command 15–25% price premiums justified by operational transparency, international brand governance, and rental yield enhancement. India ranks 6th globally for branded residence projects, with Four Seasons, Ritz-Carlton, Mandarin Oriental, and Armani partnerships across major metros. Branded residences attract premium tenant quality (expatriates, corporate executives) and offer concierge services, curated amenities, and global brand reputation that reduce operational risk—particularly valuable for NRI investors and institutional buyers prioritizing asset quality over price sensitivity[Source: Knight Frank The Residence Report 2025].

Conclusion

India’s luxury residential market stands at an inflection point historically reserved for mature developed markets. The convergence of wealth creation (UHNI population expanding 6.1% annually), institutional investor entry (pension funds, family offices, sovereign wealth allocations), international brand partnerships (branded residences ranking 6th globally), and infrastructure modernization (expressways, airport connectivity) has transformed luxury real estate from aspirational consumption into strategic asset allocation. By 2030, the market is projected to exceed USD 98 billion, representing a 70% cumulative expansion from 2025 valuations—appreciation velocity rarely sustained in maturing asset classes.

Yet this optimistic trajectory carries implicit assumptions: continued wealth creation, regulatory stability, and capital flow normality. The prudent investor recognizes that luxury real estate, while appreciating faster than mid-range residential and offering superior rental yields, remains subject to macroeconomic cycles, policy shifts, and geopolitical reorientation. The path forward demands disciplined capital deployment: geographic diversification across three-city models, branded residences allocation for operational risk mitigation, secondary market exposure for liquidity management, and ESG certification prioritization for value preservation.

YouTube Resources

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

Advertisement

Pingback: India–Sri Lanka Luxury Corridor: Strategic Investor Guide 2026