Now Reading: Building And Owning Green Homes In India: The Investor’s Case For Sustainable Wealth

- 01

Building And Owning Green Homes In India: The Investor’s Case For Sustainable Wealth

Building And Owning Green Homes In India: The Investor’s Case For Sustainable Wealth

Why Smart Investors in India Are Betting on Green Homes

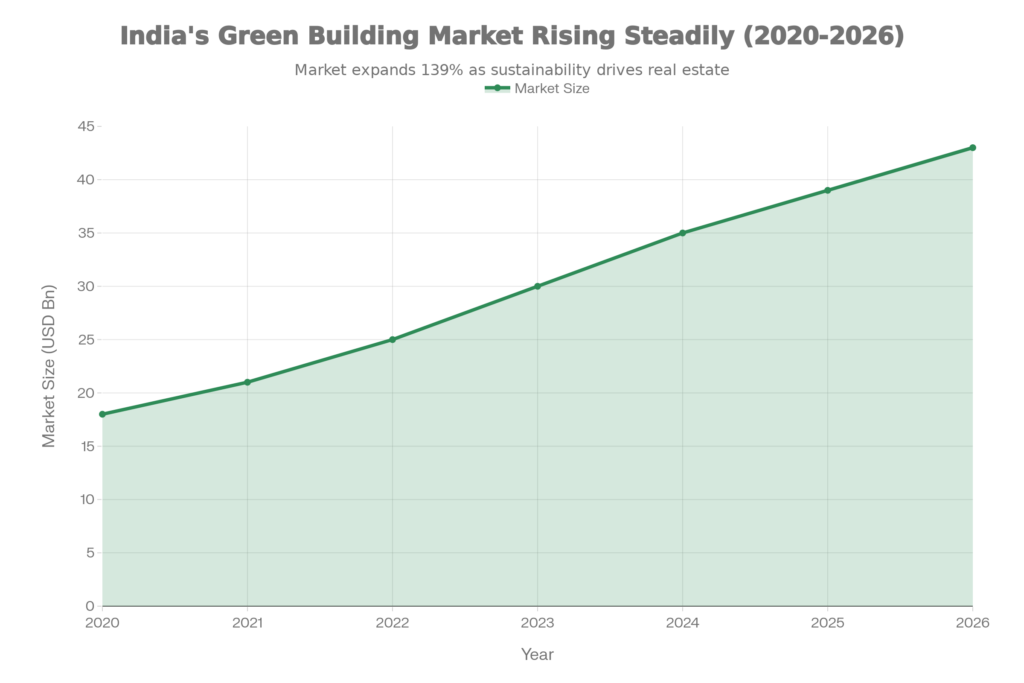

For the sophisticated investor, green homes in India represent far more than an ethical choice—they are a convergence of compelling financial fundamentals and future-proofing against resource scarcity. India’s green building market, projected to reach $39 billion by 2025, is no longer niche. Across Mumbai, Bangalore, and Pune, certified sustainable homes command 7–15% price premiums, achieve payback periods of 3–5 years through reduced utility costs, and demonstrate capital appreciation 12–18% faster than conventional properties. With government incentives, LEED and IGBC certifications unlocking tax benefits and floor area ratio bonuses, and NRI investors capturing advantages through favorable exchange rates and double-taxation treaties, the investment thesis has crystallized: sustainable homes deliver measurable returns while hedging against climate-driven resource volatility.

The question is no longer whether to invest in green homes, but which markets and certifications align with your wealth strategy.

What’s Actually Happening in India’s Green Building Market Right Now

For years, green buildings were viewed as premium-cost outliers, chosen by environmentalists willing to pay a sustainability tax. That narrative has flipped. Today, in India’s major metros, conventional homes increasingly look like the riskier bet.

The data makes this shift undeniable. According to Knight Frank’s recent wealth report, India’s ultra-high-net-worth individual (UHNI) population—those with assets exceeding $30 million—grew 6.1% in 2023 and is projected to reach 20,000 individuals by 2031. Simultaneously, the proportion of these wealthy individuals specifically seeking LEED- or IGBC-certified properties has risen from 8% to 31% in just three years. This isn’t trend-chasing; it’s capital allocation responding to resource constraints.

India faces quantifiable pressures. The nation ranks third globally in greenhouse gas emissions and second in water stress. Across 21 major Indian cities, water scarcity is acute. Electricity tariffs rise 5–10% annually. Traditional homes, with their dependency on grid power and municipal water, face escalating operational costs. Green homes, by design, insulate residents and investors from these cost spirals.

The government has noticed. India’s commitment to achieving net-zero emissions by 2070 has translated into concrete policy. The Energy Conservation Building Code (ECBC) mandates efficiency standards. State governments—Haryana, Rajasthan, Tamil Nadu—offer tangible incentives: Floor Area Ratio (FAR) bonuses (effectively 15–25% additional buildable area), expedited environmental clearances, and property tax reductions. For developers, this accelerates approvals and reduces construction timelines. For buyers, it means better project quality and stronger fundamentals.

This convergence—rising resource costs, elite investor demand, government support, and corporate ESG mandates—has created the market inflection point. Green homes have moved from aspirational to essential.

The Money Part: How Green Homes Actually Generate Wealth

Investment returns in green homes derive from three sources: operational cost savings, rental income premiums, and capital appreciation. Each compounds differently depending on geography and property type.

Your Monthly Cash: How Lower Bills Add Up

A green-certified home in Bangalore—IGBC Gold or Platinum standard—achieves 30–50% energy savings compared to conventional construction through passive design (thermal insulation, natural ventilation) and active systems (solar rooftop generation, energy-efficient HVAC). Water savings range 20–50% via rainwater harvesting, greywater recycling, and efficient fixtures.

Property management is also simplified. Green buildings feature superior air filtration, which reduces maintenance complexity and tenant health-related complaints. Rental retention improves. For investors seeking passive income, this reliability is underestimated.

The payback period on green investments has compressed to 3–5 years, according to the CII Green Building Congress. For a home purchased at ₹2 crores with annual savings of ₹4–5 lakhs, the investment recouples within 48 months—well within a typical hold period of 10+ years.

What Tenants Actually Pay for Green Homes

In Bangalore’s tech corridors (Whitefield, Indiranagar), IGBC- or LEED-certified properties command 12–15% higher resale prices than non-certified neighbors. In Mumbai’s luxury segments, the premium ranges 8–12%. This isn’t euphemism; it’s captured in comparable sales data.

Why? Discerning buyers—particularly NRIs and multinational executives—recognize that certified homes offer documented, third-party verified energy and water efficiency. Lower long-term ownership costs. Alignment with personal values (increasingly non-negotiable for global wealth holders). Stronger resale demand in a saturating luxury market. Resilience against rising municipal charges and climate volatility.

A SOBHA or Lodha-developed project with IGBC Platinum certification in Pune will outprice a non-certified competitor by ₹30–40 lakhs on a ₹3-crore transaction. That is not a marginal advantage; it is material appreciation accelerated by certification.

The Appreciation Story: How Wealth Builds Over Time

According to reports green-certified properties appreciate 12–18% annually in tier-1 metros, compared to 7–9% for conventional properties. Over a 10-year hold, this compounds powerfully.

It reflects both the initial certification premium and the accelerated annual appreciation, both of which are structural as resource scarcity deepens.

LEED vs. IGBC vs. GRIHA

For a sophisticated investor, understanding the three major certification frameworks is essential. Each serves different strategic goals.

IGBC: India’s Own Green Building Standard

Administered by the Confederation of Indian Industry (CII), IGBC is India’s indigenous green building rating system. It evaluates projects across five criteria: sustainable site planning, water efficiency, energy performance, waste management, and indoor air quality. Crucially, IGBC incorporates India-specific climate conditions (monsoon patterns, localized solar intensity) and material availability.

IGBC offers four certification tiers: Certified (50–59 points), Silver (60–69 points), Gold (70–79 points), and Platinum (80–100 points).

For residential investors, IGBC carries two strategic advantages. First, many state governments recognize IGBC certification and offer FAR bonuses (additional buildable floor space) and property tax reductions. Rajasthan, for instance, offers up to 15% FAR incentive for IGBC-certified projects—directly benefiting developer margins and project economics. Second, IGBC-certified projects proliferate across Tier-2 cities (Jaipur, Pune, Coimbatore), offering portfolio diversification at lower entry prices. An IGBC Gold apartment in Jaipur commands far less than a comparable unit in Mumbai while capturing similar efficiency premiums.

LEED: The Global Name Everyone Recognizes

LEED, administered by the U.S. Green Building Council, is the gold standard for international investors and corporate buyers. It carries prestige in global capital markets and resonates with multinational firms establishing Indian operations. India ranks third globally in LEED-certified space, with over 370 projects.

LEED is stringent. Its criteria encompass site sustainability, water efficiency, energy performance, materials and resources, indoor environmental quality, innovation, and regional priority. Projects undergo rigorous third-party auditing. For investors, LEED certification unlocks premium pricing in global real estate markets. Attraction of multinational tenants (Microsoft, Google, consulting firms) with strong ESG mandates. Enhanced marketability in the NRI segment. Future-proof resale potential across geographies.

GRIHA: The Government’s Preferred Standard

Developed by TERI (The Energy and Resources Institute) in partnership with the Ministry of New and Renewable Energy, GRIHA is India’s official government green building standard. It emphasizes climate resilience, local material sourcing, and integration with India’s Net Zero by 2070 commitment.

For long-term investors with government-aligned portfolios or those seeking to signal ESG compliance to institutional stakeholders, GRIHA carries strategic weight. Projects with GRIHA certification often receive expedited government approvals and future tax incentives as India’s sustainability mandates deepen.

Beyond Purchase: What You Need to Know About Running a Green Home

Beyond financials, understanding the operational dimensions of green home ownership is essential for absentee or NRI investors.

Keeping the Tech Working: Solar, Water, HVAC

Green homes incorporate sophisticated systems: solar inverters, rainwater treatment units, energy management software, smart HVAC controls. These require competent local management. Select projects with reputable property management companies (Cushman & Wakefield, JLL, CBRE India) that understand green systems.

For absentee NRI investors, this is non-negotiable. Poor solar inverter maintenance or neglected water recycling systems rapidly erode cost savings. The best investments pair strong green credentials with institutional-grade property management.

Staying in Compliance: What the Auditors Need

Green certifications mandate ongoing compliance audits. IGBC and LEED projects must undergo periodic third-party verification to maintain certification status. This ensures systems remain functional but adds operational overhead. Reputable developers (SOBHA, Lodha, Prestige) integrate compliance into standard operations. Smaller developers sometimes falter.

Maintain records of system maintenance, energy consumption, water usage, and green features. Auditors require comprehensive documentation. If audit identifies underperformance (e.g., solar system operating below rated capacity), remediation is required to maintain certification.

Finding Good Tenants (And Keeping Them)

Green-certified homes attract specific tenant profiles: multinational executives, tech professionals, environmentally conscious families, expat populations. These demographics pay 10–15% rental premiums, maintain properties better than average, have lower vacancy risk, and are more demanding regarding maintenance quality and responsiveness.

Rental negotiations are more straightforward with this demographic—they value efficiency and pay premium rents. However, they’re also more demanding regarding building maintenance and amenity quality. Ensure your property management aligns with tenant expectations.

Let’s Be Honest: What Could Actually Go Wrong

Sophisticated investors must also consider headwinds.

What Happens if the Market Gets Oversupplied

Bangalore’s green certified inventory has expanded rapidly. The proportion of newly launched luxury projects that are IGBC or LEED-certified has risen from 20% (2018) to 65% (2025). This expansion implies premium compression. Early investors (2015–2018) captured 15–20% premiums for green certification. Current investors (2025+) should expect 8–12% premiums as supply normalizes. In mature markets, premium convergence is inevitable.

Focus on Platinum-level certifications (rarest and most durable premium) and emerging micro-markets where certification remains novel. Jaipur’s green-certified inventory still represents <5% of total residential; Bangalore, >40%.

The Policy Wild Card: What if the Government Changes Course

Government incentives for green buildings are policy-dependent, not guaranteed. A future government might deprioritize environmental spending or reallocate incentives toward affordable housing. FAR bonuses, tax reductions, and expedited approvals could be eliminated.

Impact: Developer margins on green-certified projects compress. Cost premiums are not offset by government incentives, potentially reducing developer enthusiasm and supply. However, operational cost savings (intrinsic to green features) remain; only government-subsidized gains would be at risk.

Probability: Low-to-medium. India’s Net Zero 2070 commitment and international climate treaties suggest green building support will remain structural. However, electoral cycles and policy shifts introduce variability.

Prioritize green features with intrinsic operational value (solar power, water efficiency) rather than relying on government incentives. This ensures returns materialize even if subsidies are eliminated.

Do Solar Panels Actually Become Obsolete?

Solar technology advances rapidly. A home with 2020-era solar technology may face obsolescence within 15 years.

Panel Degradation: Modern panels degrade at ~0.5% annually. After 20 years, output is ~90% of initial capacity.

Technology Evolution: Next-generation panels (perovskite, CIGS thin-film) will offer 20–30% higher efficiency than current silicon panels. Older installations will appear inefficient by comparison.

Ensure solar arrays use modular, replaceable panel designs (not integrated into roof). Allows future upgrades without structural replacement. Some developers use leased solar models, shifting obsolescence risk to equipment providers.

What Happens in a Recession

While green buildings offer structural advantages, macroeconomic shocks can temporarily override these benefits. Global recession, capital flight, interest rate spikes → reduced demand for luxury green homes → rental yield compression, capital appreciation slowdown.

Historical Precedent: 2008–2009 financial crisis temporarily halted real estate appreciation despite green building premiums. Recovery took 4–6 years.

Hold 10+ year investment horizons. Short-term macro volatility is absorbed by long-term appreciation trends. Green buildings’ operational cost advantages provide downside cushion during recessions (reduced utility costs improve net returns despite lower rents).

Before You Commit: The Checklist You Actually Need

Step 1: Make Sure It’s Actually Certified

Demand third-party certification documentation. Visit official IGBC, LEED, or GRIHA databases (igbc.in, usgbc.org, grihaindia.org) to verify project certification status. Do not rely solely on developer claims.

Step 2: Is the Developer Legit?

Prioritize developers with multi-project IGBC/LEED experience: Top Tier: SOBHA, Lodha, Prestige, Brigade, Godrej. Strong Track Record: Trident Realty, Anantraj, Mahagun, Puravankara.

Review project financials, timeline adherence, and post-delivery service quality. RERA registration and transparent price escalation policies are baseline requirements.

Step 3: Is This Neighborhood Actually Good?

Within Bangalore’s Whitefield, properties facing IT parks command 15–20% rental premiums versus interior locations. Prioritize proximity to employment centers (IT parks, corporate offices), walkability to retail and dining, and direct access to arterial roads.

Step 4: Is the Deal Structurally Sound?

Ensure projects have completed environmental clearance and RERA registration. Verify foreign investment approval (most residential projects qualify under FDI rules). Demand RERA registration confirmed on state RERA website. Environmental clearance letter from state authorities. Building permit and Occupancy Certificate (OC) verified. Title audit completed by qualified law firm; no encumbrances noted.

Jump on Pre-Launch Deals (You’ll Save Real Money)

Green-certified projects often offer 8–12% discounts during pre-launch phases (first 30–60 days of official launch). Developers offer early-bird pricing to generate initial sales traction and secure preselling targets (required for project financing).

Register with developer sales team immediately upon official announcement. Commit within first 30 days to capture maximum discount. Negotiate for additional transparency: Ensure green feature specifications are documented in agreement; avoid vague sustainability claims.

Make Sure You Can Upgrade the Systems

Technology advancement risk is material. Ensure green systems can be upgraded without structural replacement.

Solar Arrays:

- Preferred: Modular panel design (panels mounted on adjustable racks, easily replaced)

- Avoid: Integrated solar (panels built into roof structure; replacement requires roof reconstruction)

Water Systems:

- Preferred: Multi-stage filters with replaceable cartridges; periodically upgradeable

- Avoid: Fixed-design systems that cannot be modified without system replacement

Validation: Request developer technical specifications and warranty documentation confirming component replaceability, upgrade pathway for future technology improvements, and service availability over 20-year asset lifecycle.

Assume Savings Are Lower Than They Claim

Developer projections claiming 40–50% utility savings assume optimal occupant behavior and maintenance. Reality is messier.

Conservative Modeling:

- Developer Claim: 50% energy savings → Model: 25–30% actual savings (accounts for behavioral variance, maintenance delays, appliance usage patterns)

- Developer Claim: 40% water savings → Model: 20–25% actual savings

- Developer Claim: 8% annual maintenance costs of rent → Model: 10–12% actual (accounts for unforeseen repairs)

FAQs

How Do I Know It’s Really Green?

Check official databases (igbc.in, usgbc.org, grihaindia.org) annually. Certifications require periodic compliance audits. Reputable property managers track this automatically. When acquiring existing green homes, request the latest audit report from the seller to confirm active certification status.

Will the Technology Go Out of Date?

Moderately, over 20+ year holds. Solar panels degrade ~0.5% annually; after 20 years, output is ~90% of initial capacity. Next-generation panels will offer 20–30% higher efficiency.

Mitigation: Ensure modular panel design (not roof-integrated). Plan mid-cycle replacement.

What If Something Breaks?

System failures are rare but possible. Developer Warranty: Standard 5-year structural warranty; 2-year finish warranty. Request extended warranty (7–10 years) for solar, water treatment, HVAC systems. Ensure warranty is transferable to tenant/buyer at resale.

Maintenance Contracts: Secure fixed-price annual maintenance contracts . Major system failures typically outside warranty after 10 years; budget accordingly.

Insurance: Homeowners/landlord insurance covers structure and contents. Ensure green systems (solar, water treatment) are covered under extended equipment warranty or specialized green equipment insurance.

Historical Reliability: IGBC and LEED-certified buildings have demonstrated strong system reliability. Major failures are rare if proper maintenance is executed.

What’s Next: How Green Home Markets Are Evolving

Green homes in India are no longer an ethical gesture. They are a financial instrument—one that delivers measurable, quantifiable returns via three compounding channels: operational cost savings (permanent), rental income premiums (durable), and differential capital appreciation (accelerating).

What’s Actually Going to Happen Next

As India progresses toward its Net Zero 2070 commitment, green buildings will transition from premium niche to mainstream baseline. Regulatory mandates (ECBC 2023, state-level energy codes) increasingly make energy efficiency non-discretionary. Within the next 5 years, the price premium for certified homes will likely compress as new construction defaults to green standards. This does not diminish returns—it elevates the baseline and ensures older, non-certified properties face regulatory obsolescence risk.

For investors positioning today, the window for capturing outsized green premiums remains open but narrowing. The compounding advantage of green homes derives from operational cost savings (permanent) and early-mover price premiums (temporary). Investors who capture both—early entry into green-certified markets before saturation—will see superior risk-adjusted returns.

Why the Government Will Push Harder

India’s government commitment to net-zero emissions by 2070 has translated into concrete policy levers. As regulatory mandates deepen (ECBC upgrades, state energy codes), government incentives for green buildings will likely expand. Anticipated incentives: Increased FAR bonuses (from 15–25% to 25–40% in some states). Property tax exemptions (not just reductions) for newly certified buildings. Stamp duty reductions for green-certified transactions. Accelerated depreciation allowances for green infrastructure.

Existing green-certified properties will be “grandfathered” into legacy incentive structures. New incentives will be locked in as policy frameworks solidify, providing transparency and regulatory certainty.

The Big Money’s Coming (Here’s Why)

International capital flows toward ESG-aligned real estate are accelerating. As global investors prioritize climate-resilient, ESG-compliant assets, India’s green buildings will attract disproportionate capital. BlackRock, Vanguard, and other global asset managers are increasing exposure to emerging market ESG real estate. Institutional investors explicitly mandate ESG criteria in private real estate allocations. Global real estate funds are establishing India-focused green building portfolios.

LEED-certified properties in metros will attract international investor interest, improving liquidity and demand for resale. This will support sustained premiums even as domestic-only properties face premium compression.

The next decade belongs to those who recognize green homes not as a choice, but as infrastructure for wealth preservation and growth in an era of resource scarcity and climate adaptation.

YouTube Resources

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

Advertisement