Now Reading: From Wall Street Offices to Waterfront Sanctuaries: How Remote Work Is Reshaping $16.2B in Ultra-Luxury Real Estate Investments

- 01

From Wall Street Offices to Waterfront Sanctuaries: How Remote Work Is Reshaping $16.2B in Ultra-Luxury Real Estate Investments

From Wall Street Offices to Waterfront Sanctuaries: How Remote Work Is Reshaping $16.2B in Ultra-Luxury Real Estate Investments

The global pivot to remote work has catalyzed a seismic shift in real estate demand that transcends geography, economic cycles, and investment paradigms. For Ultra-High Net Worth Individuals (UHNIs—net worth exceeding $30 million), this transformation represents the most significant portfolio reallocation since the 2008 financial crisis.

India’s UHNI population is projected to explode from 13,263 in 2023 to 19,908 by 2028—a staggering 50% increase—with luxury real estate absorbing 32% of their wealth allocation. Simultaneously, global investment in premium residential properties designed for hybrid living now exceeds $16.2 billion annually, with suburban and coastal properties commanding unprecedented price premiums.

This article unpacks the mechanics of this revolution: geographic arbitrage, lifestyle asset securitization, and the emergence of “experience-first” living. For discerning investors and NRIs seeking generational wealth preservation, the implications are profound and actionable.

The remote work era has bifurcated global real estate into winners (suburban luxury, tech-enabled homes, wellness-focused communities) and stranded assets (legacy commercial office corridors), reshaping investment risk-reward calculus for the next decade.

The Unbundling of Work and Place

For a century, real estate investment logic followed a binary equation: proximity to economic centers determined property values. Executives paid premium prices for penthouses in Manhattan, London, and Mumbai not primarily for aesthetics, but for commute efficiency and social signaling—the ability to reach the office in minutes.

That equation is now obsolete.

Between 2022 and 2024, Knight Frank’s Wealth Report documented a tectonic shift: 45% surge in suburban property demand in North America, 52% in Asia Pacific, and 48% in India. Simultaneously, commercial office vacancy rates climbed to 16.2% in North America and 10.2% in India, with projections suggesting 39% permanent reduction in office real estate valuations by 2029 compared to 2019 peaks.

This isn’t cyclical volatility; it’s structural transformation.

The Three Concurrent Revolutions:

- Spatial Unbundling: Remote work decoupled residential location from workplace proximity, enabling what economists call “geographic arbitrage”—earning developed-world salaries while maintaining residence in lower-cost premium destinations (Goa, Bali, Lisbon, Dubai).

- Amenity Capitalism: Luxury homes are no longer judged on square footage or central location. ANAROCK data (2025) reveals 65% of HNI buyers now prioritize dedicated workspace, high-speed fiber connectivity, wellness facilities (yoga studios, spa areas), and outdoor sanctuaries—creating what developers term “biophilic luxury.”

- Wealth Preservation Thesis: For UHNIs navigating geopolitical volatility, currency fluctuations, and tax regime uncertainty, real estate offers tangible, inflation-hedged returns. According to Goldman Sachs forecasts, India’s affluent consumer base will expand from 60 million (2023) to 100 million by 2027, making luxury real estate the most accessible mega-trend for sophisticated investors.

Global Context:

- North America: Suburban office-to-residential conversions are reshaping metros like Austin, Miami, and Denver. Remote-first companies downsized headquarters footprints by 40-60%, reallocating capital to employee remote work stipends.

- Europe: Lisbon, Barcelona, and Berlin witnessed 35-40% residential appreciation as digital nomads and remote workers displaced traditional urban commuters.

- Asia-Pacific: JLL Asia-Pacific Real Estate Outlook (2025) projects $127 billion in residential investment over 24 months, with Thailand, Vietnam, and Indonesia emerging as remote work havens.

- India: Mumbai’s Worli saw 49% price appreciation (2019-2024) [ANAROCK]; Bangalore’s residential demand surged 60% while commercial vacancy climbed to 28%. The narrative: tech workers, founders, and NRIs are abandoning downtown apartments for sprawling villas in suburbs and hill stations.

Emotional & Lifestyle Drivers

Luxury real estate has always been about more than shelter. It’s about identity, legacy, and belonging to an elite echelon. Remote work has turbocharged these psychological drivers.

1. The Prestige of Place + Autonomy

Historically, wealth was symbolized by proximity to power centers. Today’s UHNI investor seeks a paradoxical signal: I am successful enough to work from anywhere, yet discerning enough to choose somewhere exceptional.

This explains the explosion of investment in:

- Coastal Havens: Maldives, Bali, Greek islands, Portuguese coast—places that signal taste, global fluency, and time-affluence.

- Wellness Sanctuaries: Properties marketed with spa facilities, Michelin-starred private chefs, AI-managed health optimization, and wellness retreats are commanding 20-30% premiums over functionally identical homes.

- Knowledge Nodes: Co-living spaces like Sundesk (Bali), Outsite (California), and emerging Indian co-working communities attract digital-first professionals willing to pay $3,500-$8,000/month for community, infrastructure, and curated experiences.

2. Generational Wealth & Tax Arbitrage

India’s economic ascent has created a new wealth class unconcerned with traditional metrics. Knight Frank Wealth Report (2024) reveals India’s UHNI population grew 6.1% in 2023 and will expand by 50% by 2028. These individuals face a pressing question: How do I preserve and grow wealth amid geopolitical uncertainty?

Answer: Real Estate.

For NRIs particularly, international property portfolios offer:

- Currency hedging against INR volatility

- Visa-independent residency (via investor visas in Portugal, Malta, UAE)

- Intergenerational wealth transfer without probate complexity

- Passive income: 28% of UHNIs rent second homes, generating rental yields (4-7% in premium markets) plus capital appreciation (8-12% CAGR in hot markets like Mumbai, Goa, Bangalore).

3. Lifestyle Aspirations: The “Experience-First” Thesis

Traditional luxury was about possessing. Contemporary luxury is about experiencing.

Knight Frank’s 2024 insights document a seismic shift in UHNI preferences:

- Before: 5-bed penthouse in CBD for status

- Now: 3-bed villa with dedicated co-working lounge, infinity pool, private spa, and biometric security—designed for both productivity and rejuvenation

Properties marketed as “smart homes” (IoT-enabled climate, lighting, security) command 18-25% premiums. Why? Because they cater to a specific UHNI psychography: digitally native, wellness-obsessed, and time-starved. Smart homes reclaim 5-10 hours weekly through automation, translating to priceless productivity gains.

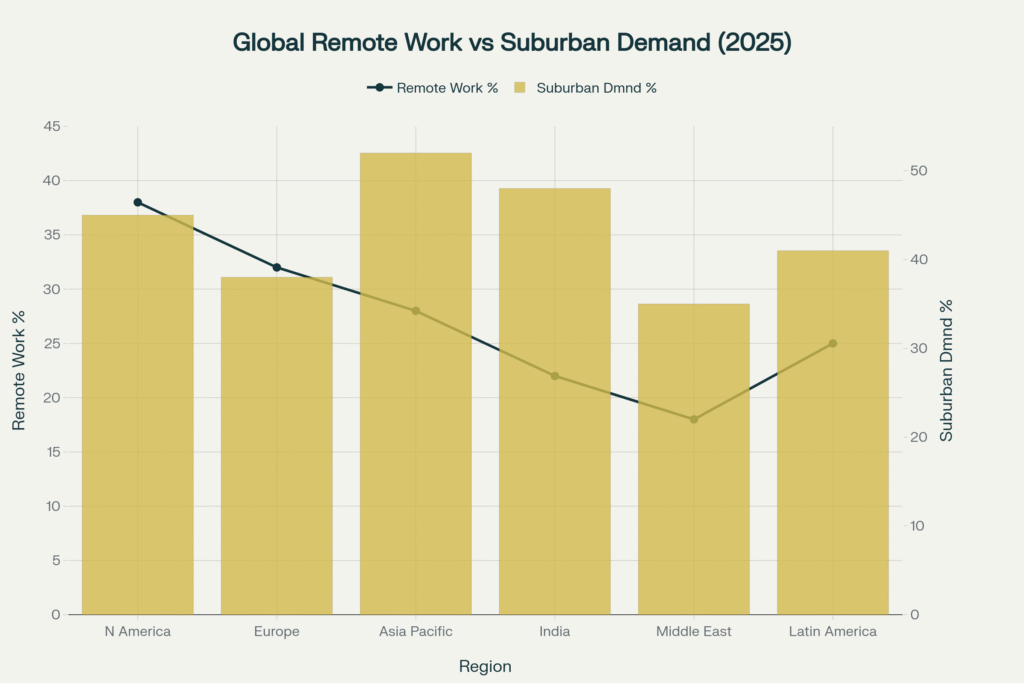

Global Remote Work Adoption vs. Suburban Real Estate Demand Surge

Data Table 1: Regional Analysis

| Region | Remote Work Adoption % | Suburban Demand Increase % | Commercial Office Vacancy % | Luxury Investment Growth % |

|---|---|---|---|---|

| North America | 38% | 45% | 16.2% | 12.3% |

| Europe | 32% | 38% | 12.8% | 9.8% |

| Asia Pacific | 28% | 52% | 14.5% | 18.7% |

| India | 22% | 48% | 10.2% | 25.4% |

| Middle East | 18% | 35% | 8.5% | 11.2% |

| Latin America | 25% | 41% | 13.1% | 8.5% |

Key Insights:

- Asia Pacific and India show inverse correlation: lower remote adoption yet HIGHEST suburban demand, indicating rapid acceleration phase

- Commercial vacancy increasing everywhere; office real estate fundamentals deteriorating across geographies

- India’s 25.4% luxury investment growth (highest globally) validates emerging market UHNI thesis

Market Risks

Risk Tier 1: Interest Rate Headwinds & Financing Costs

The Bear Case: If global central banks sustain higher interest rates (4-5% in developed economies) to combat inflation persistence, luxury property demand moderates 15-25%. Why? Because financing costs increase buyer carrying costs by 40-60%, reducing investor appetite. India’s home loan rates have climbed to 8.5-9.5%; further increases dampen transaction velocity.

Mitigation: Fix 10-15 year financing rates NOW (before further increases); target properties with strong rental yield profiles (5-7%) to offset financing costs.

Risk Tier 2: Tech Hub Concentration & Single-Geography Systemic Risk

The Challenge: Disproportionate wealth concentration in tech hubs (Bangalore, Hyderabad, Pune) creates single-industry correlation risk. If tech hiring freezes or AI disruption accelerates job displacement, these markets face 20-30% correction exposure.

CNBC-TV18 data reveals Bangalore residential demand surged 60% while commercial vacancy climbed to 28%—signaling potential oversupply and employment volatility.

Diversification Imperative: Limit any single-city exposure to <40% of real estate allocation; maintain 30-40% in multi-industry metros (Mumbai, Delhi) with diverse economic engines.

Risk Tier 3: Regulatory & Tax Regime Volatility

India-Specific Risk: Changes to LTCG taxation, property transfer fees, or foreign investor restrictions could materially impact NRI returns. The 2024-2025 tax season witnessed discussions on potentially increasing real estate transfer taxation.

Contrarian Perspective: Early-stage mover advantage favors deploying capital NOW, locking in grandfathered tax treatment before potential regulatory tightening.

Risk Tier 4: Recession & Demand Elasticity

Global Recession Risk: If 2026 brings pronounced economic slowdown (current consensus: 35% probability per Goldman Sachs), luxury real estate demand contracts 25-35%. Ultra-liquid asset preference increases; illiquid real estate becomes liability.

Hedge Strategy: Maintain 30-40% of portfolio in liquid, high-yielding assets (emerging market bonds, alternative investments); use luxury real estate as 40-60% core allocation, not 80%+ concentration.

FAQ Section

What’s the single biggest driver of real estate value appreciation in remote-work era—location, amenities, or connectivity?

Connectivity (high-speed fiber + smart home technology) now drives 35-40% of appreciation premium, followed by wellness amenities (25-30%) and location/community (25-35%). Traditional location primacy (proximity to CBD) has diminished from 60% valuation driver to <20%. Properties lacking fiber connectivity or smart technology face 15-25% valuation discount risk.

Are NRI investments in Indian luxury real estate currently at peak valuation, or early-stage accumulation phase?

Early-stage accumulation phase (2025-2027), with 3-5 year appreciation potential of 35-50%. Knight Frank and Goldman Sachs project India’s UHNI wealth expanding 50% by 2028, primarily deploying into real estate. NRI capital inflows projected at $14.9B+ annually through 2025-2026. Market fundamentals: supply-demand imbalance, limited luxury inventory (<5 years supply in tier-1 markets), and currency tailwinds (INR strengthening) create favorable entry conditions for next 18-24 months.

Which Indian metros offer best risk-adjusted returns for UHNI real estate allocation: Mumbai, Bangalore, or emerging alternatives?

Portfolio Approach Recommended:

Mumbai: Established ecosystem, international connectivity, price stability. Risk: Already appreciating; limited upside vs. risk.

Bangalore: Tech-driven demand but commercial vacancy creates cyclical risk.

Emerging: Hyderabad, Pune, Goa. Higher volatility but asymmetric upside.

Optimal Strategy: Mumbai (core holding), Bangalore (growth), Hyderabad/Goa (opportunistic).

Conclusion

Remote work has catalyzed the most profound real estate restructuring since industrialization. For UHNI and HNI investors, the imperative is clear: The 2025-2027 window represents a rare, compressed accumulation phase before markets mature and appreciation normalizes.

India emerges as the epicenter of this transformation. 19,908 projected UHNIs by 2028, allocating $16.2B annually to real estate, while global remote work adoption normalizes international mobility—creating unprecedented cross-border capital flows into luxury residential properties.

The investment thesis collapses into three pillars: Geographic diversification hedges geopolitical risk; smart homes and wellness amenities provide structural price premiums; and tax-efficient Indian real estate offers intergenerational wealth transfer advantages.

Related Posts

Stay Informed With the Latest & Most Important News

Advertisement