Now Reading: India’s Luxury Real Estate Hits Regulatory Maturity: What You Need to Know Now

- 01

India’s Luxury Real Estate Hits Regulatory Maturity: What You Need to Know Now

India’s Luxury Real Estate Hits Regulatory Maturity: What You Need to Know Now

India’s luxury property market just crossed a quiet but profound threshold. After years of RERA promises and partial enforcement, 2026 brings genuine regulatory shifts and infrastructure—systems that actually work. For UHNI and HNI investors, this isn’t just compliance theater anymore. It’s competitive advantage. Developers who execute within these new boundaries attract institutional capital. Those who don’t, fade. The old days of handshake deals and timeline ambiguity are over. Welcome to a market where execution track record matters more than glossy brochures.

When Rules Finally Got Teeth

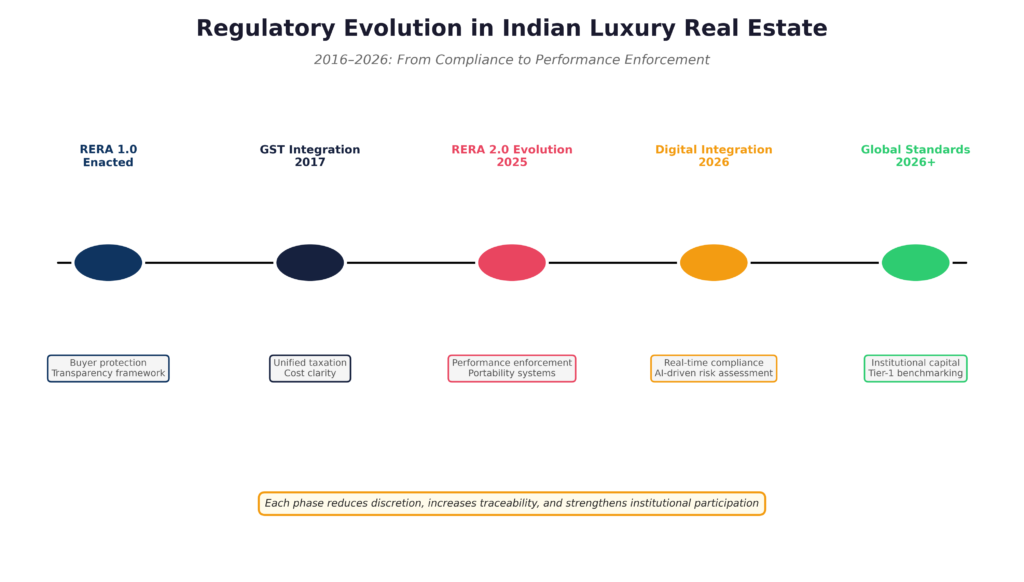

Real estate in India used to live in the space between ambition and reality. Developers announced grand projects. Buyers signed checks. Timelines stretched. Eventually, keys exchanged hands—or didn’t. The risk felt personal, bilateral. Developers controlled delivery. Investors controlled capital. Everyone knew the game. RERA changed the framing in 2016, but only partially. Projects needed registration. Escrow accounts appeared. Penalties existed on paper. But enforcement remained spotty, state by state. The system exposed problems more than it solved them.What happened in 2025 feels different. Call it RERA 2.0 or regulatory maturation—either way, it’s infrastructure now.

Digital verification of construction milestones. Real-time tracking of escrow disbursements. Penalties that kick in automatically when developers miss deadlines by 30 days. No more judgment calls. The system just works.For someone writing a big check on a Mumbai sea-facing apartment, this matters enormously. You can now pull up any developer’s penalty history, see their escrow velocity, verify structural completion certificates. What used to be lunch conversation is now public record. The power balance shifts.

Three Layers Every Serious Investor Must Navigate

Think of the regulatory landscape as three interlocking systems, each tightening the market in its own way.

First, RERA governs the developer-buyer relationship. Every project over a certain size must register upfront. Funds go into escrow. Completion milestones get third-party certification. Miss a deadline? Penalties compound at market rates. Buyers get statutory refunds with interest if they walk away. No more “let’s talk it over” when possession slips six months.

Second, FEMA and FDI rules control who can buy what. NRIs face no limits on residential purchases—welcome news for sea-view Bandra flats or Bangalore golf course villas. But farmland? Off limits. Flipping land for profit? Prohibited. Development projects welcome foreign capital, but only if you’re building something substantial. Three-year holds apply before you can transfer control. These rules channel money into long-term commitments, not short-term trades.

Third, institutional standards reshape capital flows. SEBI‘s REIT regulations demand quarterly transparency and steady dividends. Global funds must check ESG boxes. Family offices want audited track records. What used to be a domestic game now operates under international scrutiny.These layers don’t just coexist—they reinforce each other. A developer seeking institutional money needs RERA compliance. An NRI buyer wants FEMA clarity. Global funds demand both plus SEBI-grade reporting. The market sorts itself efficiently.

RERA 2.0: Regulatory Shift From Paperwork to Performance

The real shift happened when regulators stopped caring about registration certificates and started measuring delivery. RERA 1.0 caught bad actors after the fact. RERA 2.0 prevents problems before they happen.Developers now get automated warnings 30 days before deadline breaches. Extensions require formal approval or acceptance of escalating penalties. Escrow funds can’t sit idle—disbursements follow verified milestones. Completion certificates come from independent engineers, logged digitally forever.

A practical example: that long-delayed Worli tower finally nearing completion. The developer knows exactly how much each month’s delay costs in statutory penalties. Buyers know exactly when structural completion gets certified. No more “trust us, it’s almost ready.”

For investors, this creates a new due diligence baseline. Before wiring ₹20 crore, pull the RERA portal data. Has this developer ever paid penalties? How quickly do they close escrow disputes? What’s their milestone hit rate across projects? Answers that used to require private investigators now live in public databases.The market responds predictably.

Top developers who always delivered anyway see their pricing power strengthen. Marginal players who survived on delays and disputes face cash flow squeezes. Capital flows to execution capability.

NRI Pathways: Clear Rules, Firm Boundaries

Non-resident Indians face straightforward but unyielding guidelines.Direct residential purchase works smoothly. Open an NRE account, wire funds, buy the apartment. No upper price limit. A ₹50 crore Malabar Hill duplex? Perfectly legal.

REITs offer the liquid alternative. List on NSE or BSE. Buy units like stocks. Collect quarterly dividends. Clean and predictable. No property management hassles. No lock-in periods. Dividend income flows reliably while your capital stays flexible.Development projects remain the institutional play.

Foreign capital can fund townships or large apartment complexes, but minimum sizes apply. Post-completion, three-year hold before exit. Perfect for funds, cumbersome for individuals. The policy intent shines through: India wants committed capital, not flippers. Hence the trading prohibition, hold periods, and development minimums. Savvy NRIs structure accordingly.

Institutional Money Changes Everything

Luxury real estate stopped being just a rich person’s purchase a while back. Pension funds, insurance pools, and sovereign wealth vehicles now write big checks. They don’t buy on vibes—they buy data.Tier-one developers like Lodha or Sobha command premiums that reflect their compliance track records, not just their marketing budgets. A 15% price gap between a branded tower and an unproven competitor now reflects real execution differences. Paying extra for a name starts feeling like buying insurance against delays. Standardized agreements speed closings. Post-sale liquidity improves. What used to be lifestyle purchases now carry portfolio-grade attributes.

Where Geography Still Matters

Not all states execute RERA with equal seriousness.

- Maharashtra leads— Mumbai and Pune projects face the tightest scrutiny.

- Karnataka follows closely.

- Delhi-NCR splits: Delhi proper enforces rigorously, Noida less so.

- Hyderabad and Chennai lag.Smart investors arbitrage this.

Mumbai offers execution certainty at peak pricing. Hyderabad tempts with discounts but carries regulatory uncertainty. Bangalore splits the difference.The gaps will narrow. NITI Aayog pushes uniform standards. But for now, geography remains a legitimate variable in risk-adjusted pricing.

Risks Worth Losing Sleep Over

Regulation improves, execution risk persists. Steel prices doubled. Skilled labor vanished. Environmental clearances drag. RERA penalties compensate but don’t eliminate opportunity costs.Interest rates matter more than ever. Most buyers leverage—even UHNIs. RBI hikes turn comfortable EMIs into stressors. Policy can shift. Three-year lock-ins become five. REIT dividends face new taxes. Unlikely, but model the tail risks. Ultra-luxury supply accelerates. Without sustained NRI inflows, absorption slows by 2028.

FAQs

How does RERA 2.0 actually differ from the original RERA in practical terms?

RERA 1.0 reacted to delays with after-the-fact complaints. RERA 2.0 prevents them—developers get 30-day automated warnings before penalties start compounding automatically. Timeline slippage now carries immediate financial consequences.

What’s the minimum investment needed to meaningfully participate in India’s luxury real estate market?

Around ₹5 crore gets you into trophy-quality assets from reputable developers in Mumbai or Bangalore. Below that threshold, REITs offer better diversification and liquidity without property management hassles.

Which cities offer the best balance of regulatory certainty and pricing for 2026 investments?

Mumbai provides maximum RERA enforcement but peak valuations. Bangalore offers strong execution with better entry pricing. Hyderabad tempts with 15-20% discounts but carries higher regulatory risk. Arbitrage exists while state-level enforcement converges.

Conclusion

India’s luxury real estate market has quietly crossed a threshold that reshapes everything. RERA 2.0 isn’t just another regulation—it’s infrastructure that endures. Developers who once thrived on timeline ambiguity now face binary choices: execute within the system or watch institutional capital flow elsewhere. The compliant few command pricing power that compounds.

For UHNI and HNI investors, this maturity creates rare clarity. Execution risk becomes measurable through public penalty ledgers and milestone data. Developer quality overtakes location as the primary variable. NRI pathways—direct residential, REITs, selective development—offer tax-efficient structures that reward strategic positioning over speculation. Discerning investors act now, not later. Verify track records. Structure tax-efficiently. Compliance isn’t a checkbox anymore—it’s the foundation where wealth concentrates.

YouTube Resources

Free Resources To Download

India Luxury Real Estate 2026:Key Regulatory Shifts