Now Reading: COVID-19 Reshaped Indian Luxury Housing: Why HNI/UHNI Investors Should Act in 2026

-

01

COVID-19 Reshaped Indian Luxury Housing: Why HNI/UHNI Investors Should Act in 2026

COVID-19 Reshaped Indian Luxury Housing: Why HNI/UHNI Investors Should Act in 2026

The COVID-19 pandemic fundamentally rewired Indian luxury housing demand, transforming what had been a transaction-driven market into a lifestyle-driven one. Between 2020 and 2025, India’s real estate sector experienced a seismic shift: affluent buyers abandoned compact urban flats for spacious, amenity-rich properties in prime locations. Today, premium residential assets (₹1 crore+) capture around 62% of housing sales—up from just 44% pre-pandemic.

This structural shift accelerates in 2026, the inflection year when three forces converge: India’s UHNI population reaches 19,908 (a 50% increase since 2023), institutional capital flooding real estate ($5-7 billion projected), and luxury segment sales compounds at 12-15% CAGR. For UHNI/HNI investors, 2026 marks the window to acquire premium assets before price acceleration outpaces institutional investment capacity. Investors delaying decisions beyond Q2 2026 risk entering a market where fundamental demand has permanently shifted, and pricing has recalibrated to reflect new wealth paradigms.

The Pandemic Shock That Never Reversed

When India locked down in March 2020, real estate transactions collapsed in Q2 2020 compared to Q1 2020. Housing finance dried up. Developers froze launches. Buyers retreated. On the surface, the story seemed one of cyclical downturn. But beneath lay permanent disruption.

Families working from home discovered something extraordinary: their 900-square-foot Mumbai flat wasn’t a luxury; it felt like a cage. The guest bedroom became a second office. The living room transformed into a gym. The terrace—forgotten for years—suddenly hosted morning meditation and evening aperitifs. For the first time in modern urban India, space became currency. Not proximity to office. Not transit access. Space. Air. Greenery. Possibility.

This realization didn’t evaporate when lockdowns ended. If anything, it crystallized. By 2024, the preference had calcified into structural demand: 51% of residential transactions involved properties priced above ₹1 crore—up from 44% in 2023. Among HNIs and UHNIs, the shift was more dramatic still. Luxury segment sales (₹4 crore+) grew 37.8% year-on-year in the first nine months of 2024, reaching 12,625 units compared to 9,160 the prior year.

This wasn’t a speculative bubble. It reflected a permanent repricing of what affluent Indians valued: wellness-integrated homes with dedicated fitness zones, outdoor terraces designed for working, temperature-controlled libraries, wine cellars, smart automation systems, and crucially, distance from urban density. The pandemic didn’t create this demand; it revealed it. And Indian developers—from established names like Lodha and Prestige to newer entrants like Adani Realty—have spent the past three years building to satisfy it.

The Global Context: Why Now?

India’s housing transformation occurs within a larger macroeconomic narrative. Globally, ultra-high-net-worth individuals (those exceeding $30 million in assets) are concentrating wealth at unprecedented rates. Across developed markets, regulatory friction, wealth taxation, and political uncertainty have made property ownership less attractive. Not in India.

India ranks among the world’s fastest-growing wealth markets. The UHNI population grew 5.6% in 2023 alone. By 2028, Knight Frank projects this will expand to 19,908 UHNIs—a 50% increase. No other major economy (except mainland China at 47%) comes close to this growth trajectory. This isn’t abstract GDP expansion; it translates directly into real estate demand. ANAROCK research indicates 20% of newly created UHNIs plan residential property acquisitions within 18 months of wealth creation. For HNIs, the figure is even higher: over 30% plan luxury real estate purchases within two years.

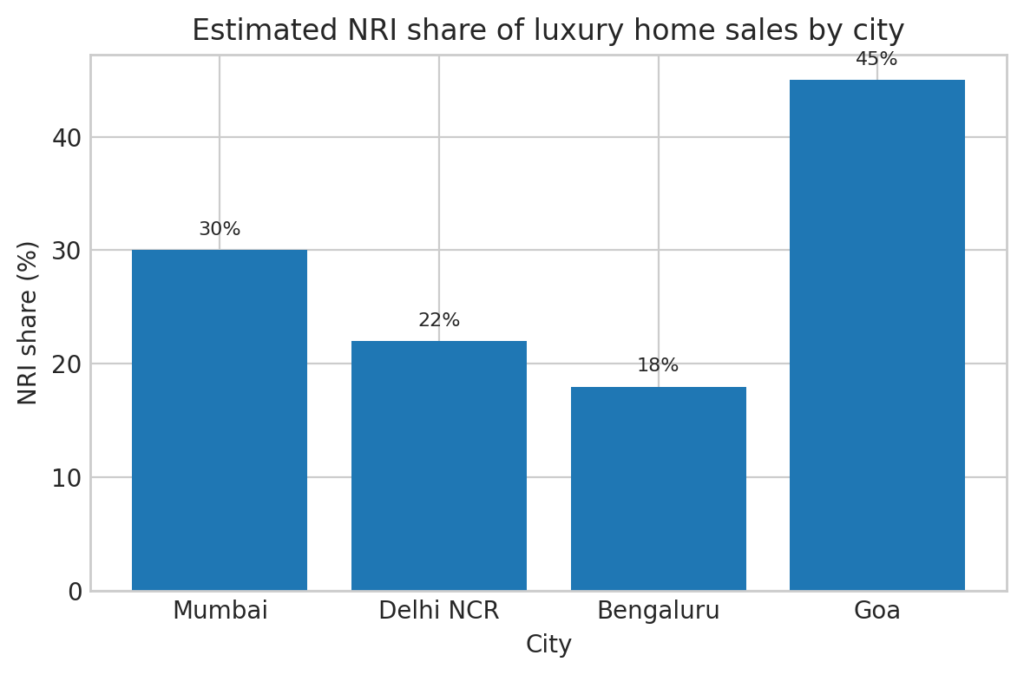

Simultaneously, NRI (Non-Resident Indian) capital has discovered Indian real estate as a stable, tangible hedge. With rupee appreciation against major currencies, NRIs are deploying capital strategically. Anarock projects NRI investments in Indian real estate will reach USD 14.9 billion by 2025—a 20% year-on-year increase. The bulk targets luxury residential assets in Mumbai, Delhi-NCR, and Bengaluru, where global brand recognition and lifestyle infrastructure attract international capital.

Emotional & Lifestyle Drivers: The New Calculus

Numbers alone don’t capture the psychological shift. Speak with HNI buyers across metros, and a pattern emerges: property is no longer about ROI or resale value alone. It’s about experience.

Post-pandemic affluent buyers expect homes to function as private wellness retreats, home offices, entertainment venues, and generational assets simultaneously. A ₹5-crore Mumbai apartment isn’t just shelter; it’s a statement of identity and a hedge against urban chaos.

This explains the surge in demand for specific amenities: spa zones, yoga decks, meditation gardens, air purification systems, organic waste management, and integrated smart home automation. Prestige Group’s luxury launches in Bengaluru now include dedicated meditation rooms and temperature-controlled wine cellars. Lodha’s Mumbai projects feature rooftop infinity pools overlooking the Arabian Sea, helipad access, and private spa suites. These aren’t luxuries; they’re now table-stakes.

NRIs driving this shift report a secondary motivation: portfolio diversification outside home countries. With geopolitical uncertainty in the West and immigration-related policy volatility, Indian real estate offers stability, liquid resale potential, and emotional connection to homeland. For the diaspora, a ₹3-5 crore apartment in Mumbai Worli or Delhi’s Aravalli Residency represents three things: a vacation home, a retirement nest egg, and a tangible link to family roots.

Younger HNIs (those under 45) emphasize sustainability and ESG alignment. They seek properties with LEED or IGBC Green Building certification, renewable energy systems, and water recycling infrastructure. This cohort represents 35% of new luxury purchases and is driving architectural innovation toward biophilic design and carbon-neutral construction.

Indian Luxury Housing Sales by City (9M 2023 vs 9M 2024)

| City | 9M 2023 | 9M 2024 | YoY Growth | % Change |

|---|---|---|---|---|

| Delhi-NCR | 3,410 | 5,855 | 2,445 | +72% |

| Mumbai | 3,250 | 3,820 | 570 | +18% |

| Pune | 330 | 810 | 480 | +145% |

| Hyderabad | 630 | 200 | (430) | -68% |

| Bangalore | 240 | 35 | (205) | -85% |

| Kolkata | 50 | 80 | 30 | +60% |

| Total | 9,160 | 12,625 | 3,465 | +37.8% |

Source: CBRE India Market Monitor Q3 2024

Insight: Delhi-NCR’s explosive 72% growth reflects accelerated institutional investment and strong NRI demand, while traditional IT hubs (Bangalore) saw consolidation. Pune’s 145% surge indicates Tier-1+ city emergence, driven by better lifecycle value and lower entry points than metros.

Case Study 1: The Delhi-NCR Institutional Capital Surge

Delhi-NCR’s 72% luxury sales growth (2024) is no accident—it’s institutional strategy. The National Capital Region has emerged as the primary target for family offices and alternative investment funds seeking residential real estate exposure.

The Catalyst: The Jewar Airport project, operational by 2026, plus the Yamuna Expressway corridor development, has triggered infrastructure-driven appreciation. Luxury properties in Gurgaon’s Golf Course Road, South Delhi’s Aravalli Residency, and Noida’s Sector 150 are capturing institutional capital seeking 12-15% annual appreciation.

Key Players:

- Lodha Group‘s Gurgaon residencies attracting $2-3 crore commitments from family offices

- Adani Realty launching Zen estates in Noida with sold-out pre-launch units

- Omaxe and Mahagun targeting NRI allocations through Dubai distribution partnerships

Investment Profile:

- Entry price: ₹2-5 crore for 3-4 BHK luxury apartments

- Expected 5-year appreciation: 40-50%

- Rental yield: 2.5-3.5% (below national average, but capital appreciation compensates)

- Liquidity: 9-12 months for quality properties in prime locations

Why It Matters: Delhi-NCR’s surge reflects investor confidence in infrastructure-linked wealth creation. Unlike speculative markets, institutional capital targeting Delhi-NCR focuses on 7-10 year hold horizons, indicating structural, not cyclical, demand. For HNIs, this means early institutional commitment validates fundamental demand, reducing investment risk.

Case Study 2: Mumbai’s Persistent Premium Dominance

Mumbai remains India’s luxury real estate capital, not by spectacular growth (18% YoY), but by durability. While Delhi-NCR surged, Mumbai sustained demand through consistent buyer preference and global brand recognition.

The Shift: Luxury buyers in Mumbai are increasingly drawn to peripheral premium locations—Thane’s Lodha Amara, Chembur’s Runwal residencies, and Worli’s waterfront projects—rather than central business districts. This reflects the post-pandemic flight toward space and tranquility.

Case in Point:

- Lodha’s Thane waterfront project recorded pre-launch demand exceeding ₹500 crore within weeks

- Average unit size increasing from 1,200 sq ft (2019) to 1,800-2,200 sq ft (2024)

- Price per sq ft stabilizing at ₹2.5-3.5 lakh in premium segments

NRI Component: Mumbai captures 35% of NRI investments into Indian residential real estate, according to ANAROCK data. Diaspora seeking second homes, retirement assets, or wealth diversification drives consistent demand even when domestic appetite cycles downward.

Investment Profile:

- Entry price: ₹3-7 crore for 2-3 BHK waterfront/peripheral premium

- Expected appreciation: 5-8% annually

- Rental yield: 2-2.5%

- Liquidity: 6-9 months for institutional-grade properties

Why It Matters: Mumbai’s stability masks supply-side constraint that will intensify by 2027. Limited redevelopment opportunities in central areas and high FSI saturation mean future supply concentration in peripheral premium zones—a tailwind for early investors.

Case Study 3: Pune’s Emergence As HNI Secondary Hub

Pune recorded 145% luxury sales growth in 9M 2024 (from 330 to 810 units)—the sharpest growth among metro-adjacent cities. This reflects institutional capital repositioning toward Tier-1+ cities offering better value multiples and lifestyle amenities.

The Opportunity:

- Entry prices 40-50% lower than Mumbai for equivalent quality

- Vibrant startup ecosystem (similar to Bengaluru pre-2015) attracting first-generation UHNIs

- Large NRI community from the US (Pune alumni diaspora via educational institutions)

- Growing luxury infrastructure: malls, hospitals, educational institutions, cultural venues

Case in Point:

- Prestige Group’s luxury projects in Pune’s IT corridor recording 80% pre-launch bookings

- Average price appreciation: 8-12% annually (vs. 6-8% in Mumbai)

- Senior living and alternative asset development (co-living, student housing) creating ecosystem depth

Investment Profile:

- Entry price: ₹1.5-3.5 crore for premium 2-3 BHK

- Expected 5-year appreciation: 45-60%

- Rental yield: 3-4% (superior to Mumbai)

- Liquidity: 8-12 months (slightly extended vs. metros)

Why It Matters: Pune represents the “second-wave” capital allocation opportunity. As Delhi-NCR and Mumbai face supply constraints and price normalization, institutional capital is systematically deploying to Tier-1+ cities with superior value-to-appreciation ratios. For HNI investors seeking 12-15% annual returns, Pune offers the last tranche of high-growth cities before market maturation.

Risks & Contrarian Perspectives

The Regulatory Headwind

India’s real estate sector, despite liberalization, remains subject to significant regulatory friction. The Real Estate (Regulation & Development) Act, 2016 created clarity but also raised compliance costs. State-level stamp duty variations (ranging 4-9% across metros) and GST implications for under-construction properties add transaction drag. A change in tax policy—such as an increase in capital gains taxation or wealth taxation—could compress valuations by 10-15%, particularly in speculative segments. Investors should monitor 2026 budget announcements (typically February) for fiscal policy signals.

Supply-Side Overshoot in Tier-2 Cities

While Tier-2 cities offer attractive value, some markets (Jaipur, Surat, Indore) risk oversupply if institutional capital floods simultaneously. Unlike metros with constrained supply, emerging cities may see inventory multiply rapidly, compressing appreciation. Investors should verify absorption rates and pre-launch booking momentum before committing to secondary cities.

Global Recession Contagion

India’s real estate appreciation is underpinned by wealth creation from global business services, IT exports, and diaspora capital. A significant global recession (2-3% contraction in developed markets) could suppress NRI capital flows by 15-20% and reduce first-gen UHNI wealth creation by 8-10%, moderating demand. The sector has proven resilient during 2008 and 2020 crises, but concentrations of debt in under-capitalized developers pose residual risk.

FAQs

What is the realistic price appreciation timeline for luxury residential properties in India’s top metros in 2026?

Based on current institutional capital deployment and demographic projections, expect 7.5% price appreciation in 2026, accelerating to 8-12% annually in 2027-2028. Delhi-NCR may outpace this at 10-12%, while Mumbai stabilizes at 6-8%. Tier-2 cities could see 10-15% appreciation if institutional capital allocation intensifies.

Should HNI investors prioritize capital appreciation or rental yield when selecting luxury residential assets in 2026?

Prioritize capital appreciation in 2026-2027. Luxury residential yields (2-3.5% nationally) remain suboptimal compared to bond yields or equity dividend strategies. The fundamental draw is structural appreciation driven by wealth creation and supply constraint. Rental yield strategy becomes viable when pricing normalizes and institutional capital deployment matures, potentially shifting focus to income generation over appreciation.

What is the optimal investment horizon for luxury residential properties in India to maximize risk-adjusted returns?

Institutional investors typically employ 7-10 year hold horizons. This horizon captures three appreciation cycles (2026-2028 wealth creation surge, 2028-2030 supply normalization, 2030-2033 next-generation wealth consolidation). HNI individual investors should adopt 5-7 year minimum holds to absorb transaction costs (buyer’s 8-9% including registration, seller’s 2-3%) and amortize acquisition friction.

Conclusion

The COVID-19 pandemic, in retrospect, accelerated a transition that India’s wealth creation would have eventually demanded. The shift from transaction-driven to lifestyle-driven housing demand reflects something deeper: the emergence of a global-caliber affluent class with expectations shaped by international living standards.

By 2026, this transformation crystallizes into three observable facts. First, India’s UHNI population will have grown to 19,908—a permanent expansion of domestic capital seeking institutional-grade residential assets. Second, foreign capital (NRI + institutional) will have stabilized at $5-7 billion annually, replacing speculative foreign investment with patient, structural capital. Third, supply in premium segments will have become constrained, as developers reallocate to luxury (higher margins, higher velocity) from mid-range segments, creating positive pricing dynamics for early investors.

For UHNI and HNI investors, 2026 is not simply another vintage year; it’s a structural inflection. The window to acquire premium residential assets before price discovery reflects new wealth paradigms will close by mid-year. After that, investors entering the market face two headwinds: normalized pricing reflecting institutional valuation models and compressed inventory in primary locations.

YouTube Resources

Related reading: Smart home investment guide — ROI, system tiers, and what to look for when buying — NRI real estate investment guide — legal framework, financing, and market selection.

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post